UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANY

Investment Company Act file number 811-07074

| | |

| 180 DEGREE CAPITAL CORP. |

| (Exact Name of Registrant as Specified in Its Charter) |

| | | | | | | | |

| 7 N. Willow Street, Suite 4B, Montclair NJ | | 07042 |

| (Address of Principal Executive Offices) | | (Zip Code) |

| | |

Daniel B. Wolfe

President and Chief Financial Officer

180 Degree Capital Corp.

7 N. Willow Street, Suite 4B

Montclair, NJ 07042 |

| (Name and address of agent for service) |

|

Copy to:

John J. Mahon, Esq.

Schulte Roth & Zabel, LLP

1152 Fifteenth Street, NW

Suite 850

Washington, DC 20005

(202) 729-7477 |

Registrant's telephone number, including area code: (973) 746-4500

Date of fiscal year end: December 31

Date of reporting period: June 30, 2020

Beginning on January 1, 2021, and as permitted by a rule adopted by the Securities and Exchange Commission ("SEC"), paper copies of the shareholder reports of 180 Degree Capital Corp. (the "Company") like this one, will no longer be sent to you by mail unless you specifically request that your financial intermediary (i.e., the broker-dealer or bank through which you own your shares) or the Company, as applicable, send you paper copies. Instead, shareholder reports will be made available on a website, and you will be notified by mail each time a report is posted and you will be provided with a website link to access the report.

If you already have elected to receive shareholder reports electronically, you will not be affected by this change and need not take any action. You may elect to receive all future shareholder reports of the Company in paper free of charge. If you own shares through a financial intermediary, you may contact your financial intermediary to elect to continue to receive paper copies of your shareholder reports, or if your shares are not held by a financial intermediary, you may contact the Company's transfer agent, American Stock Transfer & Trust Company, LLC at 800-937-5449, or the Company at 833-293-1769.

Item 1.

Fellow Shareholders,

Samuel Beckett’s classic play, Waiting for Godot, is the story of two characters, Vladimir and Estragon, who are engaged in the endless drivel of inane conversations and activities all while waiting for the mysterious “Godot”- a man who will supposedly save them by giving them food and a place to sleep. For those who are not familiar with or who have not seen the play, I apologize for spoiling the ending… He never comes. Essentially, Beckett’s masterpiece is a story describing the human condition of waiting for something to happen that never will. For many years, our business was solely focused on venture capital investments and our shareholders suffered through years and years waiting for monetization events with superior returns. The monetization events were few and far between, and there was no alternative strategy to create value for our shareholders. In 2016, we devised a new strategy of investing in the public markets focused on our micro-cap activism. Simply put, unlike Vladimir and Estragon, we no longer wanted 180 to be dependent on outside forces for which we have little control. The good news on that front is that we have been able to grow our book value because of our public stock picking. The better news for us this past quarter is, surprisingly, Godot showed up in the form of a monetization event of Petra Pharma Corporation, one of our private holdings. This past quarter, Petra was sold to an undisclosed buyer. Between our direct ownership in Petra and our indirect ownership through Accelerator IV-New York Corporation, we received approximately $4.7 million in cash, approximately $350,000 in potential additional proceeds held in escrow for one year from the close of the transaction, shares in a new spinout company that are fair valued at approximately $110,000, and the potential for future payments upon achieving development and business milestones of up to approximately $86.9 million. We fair valued the potential future milestone payments at approximately $6.4 million as of the end of this quarter. Largely driven by Petra, our private portfolio was up 30.6% and grew our book value by $0.34 per share. On the public side, our gross total return of 23.9% was solid on an absolute return basis, was mixed in relation to the Russell Microcap Index increase of 30.5% and the Russell Microcap Value Index 22.7%.

The primary difference with how we view our private portfolio today versus years ago needs to be discussed. It is not that we were ever sour on our private holdings, or that we didn’t believe in them. It was simply that we had and continue to have limited control over the duration it would take to monetize the investments. When coupled with the facts that: 1) we had no other strategy (versus today’s public markets focus); 2) we had annual operating expenses that were nearly 8% of assets (versus half that today); and 3) we had limited cash and securities of publicly traded companies ($17.1 million, net of debt, as of the end of Q2 2016, versus $44.6 million, and no debt as of the end of the Q2 2020), we were headed down a path where we were going to be forced into selling positions we didn’t want to sell. Forced liquidations would prove destructive to value for our shareholders. For an investor, there is a big difference between “wanting” to sell and “having” to sell. Unlike four years ago, we now have a balance sheet which provides us the luxury of seeing our private holdings through to their natural conclusions. And today, we are in a position where our shareholders can benefit from an acquisition of Petra. In the last 3.5 years alone, we have monetized Mersana, HZO, and now Petra for values greater than their NAV marks. At 180, we don’t sit idly waiting for Godot; but it is really nice when he/she shows up! We had a great quarter of NAV growth of 27.4%.

In terms of the public markets, what can I possibly add that hasn’t been repeated? I have lived through many a bear market, but I’ve never invested through a pandemic. The question from the beginning is when will normalcy return. In my view, there is an expiration date on COVID-19 and a return to some sense of normalcy – that expiration date is likely when we have an effective vaccine. The speed at which we contain the virus, find therapeutics for the virus, ensure testing for the virus, and find a vaccine for the virus will determine how quickly the economy can rebound and how the market performs over the course of the next year. I see both sides of the bull/bear debate. The bear case is that the virus is incredibly lethal in certain people, is highly contagious, and will be with us for a very long time without a vaccine. The bull case is that the market has already adjusted to that, we are starting to leave our homes again, therapeutics are coming, and a vaccine is on its way. Following the collapse of the stock market in March, the market began to recover following massive fiscal and monetary stimulus programs. This past quarter, the economy began to re-open as cases of COVID-19 flattened across many of the states that were hit hard early on (e.g. New York and New Jersey). I think we will continue to see sudden shocks to the economy depending on the number of waves of the virus. Presently, we are seeing Florida, Texas, Arizona, California, and Georgia suffering through the same vicious outbreak of COVID-19 cases that earlier, hard-hit states experienced.

So many questions linger unanswered: Will we have to shut down again? Will schools open? Will restrictions be lifted on restaurants? Will sports return and, if so, for how long? Will more stimulus be needed? At what capacity will air travel resume? One of my favorite books is Freakonomics by Steven Levitt and Stephen Dubner, which studies the riddles of everyday life through an economics lens. In the introduction of the book, it is noted that “Levitt’s underlying belief that the modern world, despite a surfeit of obfuscation, complication, and downright deceit, is NOT impenetrable, is not unknowable, and -if the right questions are asked- is even more intriguing than we think.” Is there any greater riddle than trying to figure how the world, the stock market, and the economy are going to play out on a day to day basis?

Here is how 180 seeks to ask the right questions. For my whole career, I have tried to take the complexities of investing and boil them down to the one or two things that actually matter. For us, that is the notion that the price that we pay for a business will be the predominant determining factor in driving investment returns. Of course, you need catalysts and alpha generating management teams to coincide with just buying “cheap” stocks; our unwavering Graham Dodd value approach forces us to focus on buying good companies at the right price at the right time. Through all the uncertainties of the world we live in, we believe having that micro-focus on a select few companies will give us the greatest chance of creating significant value for 180’s shareholders.

It is so easy to preoccupy my time trying justify in my head how, for example, in the middle of a pandemic, the Nasdaq 100 index is up 28% (through August 5, 2020… more on this later). Why should I care about that? I don’t care in as much as that question has no relevance to how we are going to create value for 180's shareholders. We spend our time only on the things that mater for 180 and its shareholders. What I care about are making sound investments, using our activist influence, and looking for companies that we believe have the potential for 100% or greater returns in about 3 years. The “right question” for us is not, “Where is this market are going to be in the next three minutes?”, or "Have you seen how much the QQQ Index is up?" The questions for us are, "What is SONM going to be earning in two years?" and "Do I think QMCO can grow its topline by over 50% in the next three years?" That might sound Pollyannaish and it could come across as being naïve to the nasty environment or macro issues that affect the markets. It is neither. We are simply very disciplined about our process, know what characteristics we are looking for in a company, and when we find one, we make it a big holding. It is how I have viewed investing since 1988, and hopefully will accrue to the benefit for all 180’s shareholders. So, after reviewing our change in NAV for the quarter, let’s spend the time talking about our individual companies.

NET ASSET VALUE PER SHARE

Our net asset value per share (“NAV”) increased this quarter from $2.12 to $2.70. Our Fund has three principal components to the variance in our NAV: our public portfolio, our private portfolio, and our expenses. For the quarter, our public portfolio companies increased our NAV by $0.27, while our private portfolio companies increased our NAV by $0.34. Operating expenses decreased NAV by $0.03.

| | | | | | | | | | | | | | | | | |

| Quarter | YTD | 1 Year | 3 Year | Inception to Date |

| Q2 2020 | Q4 2019-Q2 2020 | Q2 2019-Q2 2020 | Q2 2017-Q2 2020 | Q4 2016-Q2 2020 |

| | | | | |

| | | | | |

| Change in NAV | 27.4% | (11.8)% | (4.3)% | 10.7% | 15.4% |

| | | | | |

| Russell Microcap Index | 30.5% | (11.2)% | (4.8)% | 2.6% | 7.0% |

| Russell Microcap Value Index | 22.7% | (21.4)% | (14.9)% | (8.8)% | (6.4)% |

| Russell 2000 | 25.4% | (13.0)% | (6.7)% | 6.1% | 11.4% |

Public Portfolio

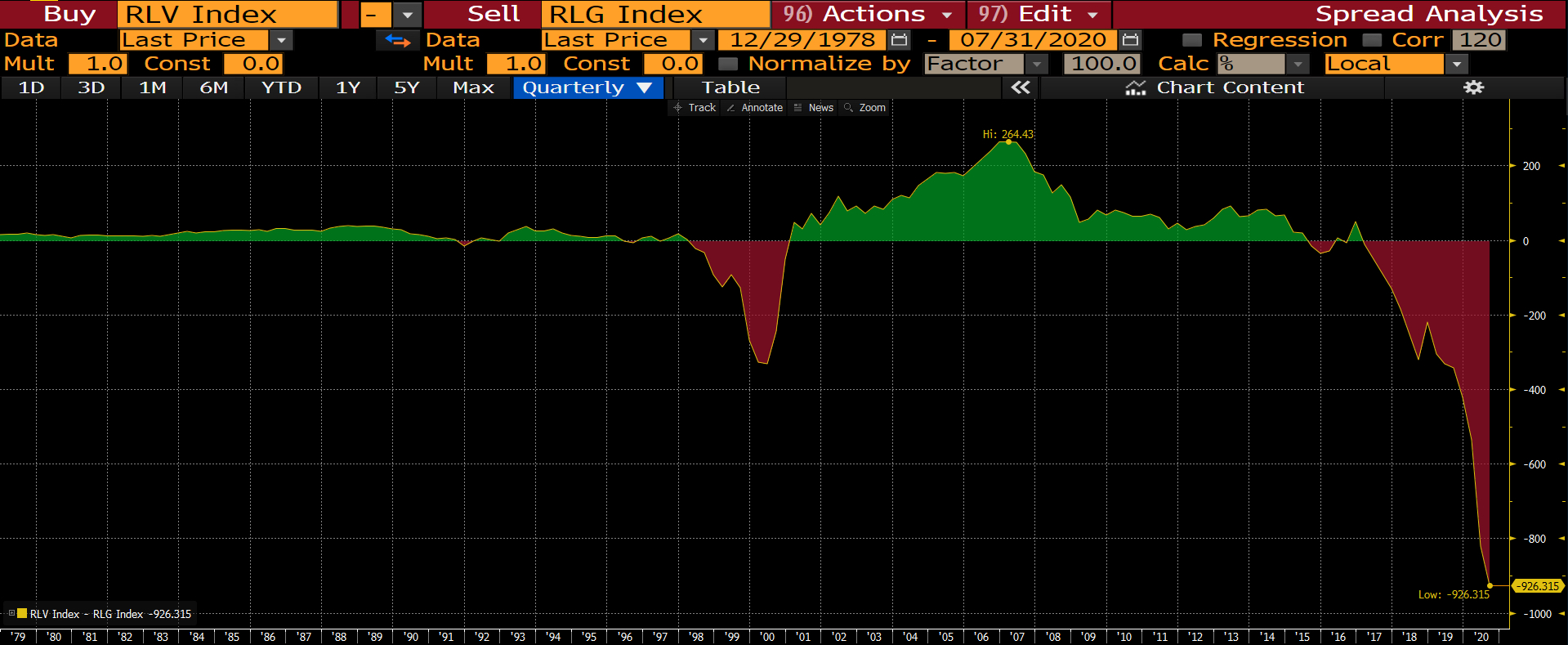

While we achieved a +23.9% gross total return, that was a mixed result relative to the Russell Microcap Index (+30.5%) and the Russell Microcap Value Index (+22.7%). I’ve never seen greater bifurcation of performance for the US Stock Market. For example, as of the end of July 2020, the Invesco QQQ (which tracks the Nasdaq 100) is +25.5% year to date while the Russell 2000 (which tracks mid-and small-cap stocks) is -10.6%. The Russell 1000 Growth Index is +18.3%, while the Russell 1000 Value Index is -13.0% year to date. We have seen the same discrepancy against the two indices we use to benchmark our performance. As of the end of July 2020, the Russell Microcap Growth Index is +5.7% while the Microcap Value Index is -21.7%. The differing returns are staggering. I mention this to serve as factual information because as you know, we play in the value sandbox of the market. While it is understandable that investors have gravitated towards those companies least impacted by COVID-19 (essentially large growth companies), the valuation discrepancy has never been so extreme as shown in the below screen.

Source: Bloomberg

Us value investors painfully lived through the all-of-nothing tech bubble back in 2000. As a matter of relative performance, the current period of draconian outperformance by the QQQ Index has led to an even greater disparity of performance between growth and value than the tech bubble by a factor of 3. As I said, I understand how we have gotten here given the meltdown of the economy. During periods like this, investors gravitate towards those companies showing growth. But I have also seen how it ends when investors pour money into only a select few companies. If and when this economy moves down the path of sustained recovery, there may be a huge catch up trade for the type of companies we invest in.

In the chart below, you see not only our quarter to date performance, but also our one year, three year, and inception to date performance. Fortunately, since the inception of 180, our focus on investing in publicly traded companies with our constructive activist approach has generated significant returns in that portion of our investment portfolio.

| | | | | | | | | | | | | | | | | |

| Quarter | YTD | 1 Year | 3 Year | Inception to Date |

| Q2 2020 | Q4 2019-Q2 2020 | Q2 2019-Q2 2020 | Q2 2017-Q2 2020 | Q4 2016-Q2 2020 |

TURN Public Portfolio

Gross Total Return | 23.9% | (14.3)% | 18.2% | 121.8% | 166.2% |

| | | | | |

| | | | | |

| | | | | |

| Russell Microcap Index | 30.5% | (11.2)% | (4.8)% | 2.6% | 7.0% |

| Russell Microcap Value Index | 22.7% | (21.4)% | (14.9)% | (8.8)% | (6.4)% |

| Russell 2000 | 25.4% | (13.0)% | (6.7)% | 6.1% | 11.4% |

Through the first month of Q3 2020 quarter, the gross total returns of our public portfolio is +11.7% versus +1.1% for the Russell Microcap Index and -0.4% for the Russell Microcap Value Index. For the year through July 31, 2020, our -4.3% gross total return beats both the Russell Microcap (-10.3%) and the Russell Microcap Value Index (-21.7%).

Let’s dig into the significant sources of the changes in value and some brief comments for our public portfolio in Q2 2020. We will then dig in on our latest new position, Sonim Technologies, Inc., in greater detail.

Sources of material increases in value:

•Quantum Corporation (NASDAQ:QMCO) renegotiated the covenants on its outstanding debt that provided increased operating flexibility and reduced investor concern over default risk. Hyperscaler customers are returning to purchasing, albeit not at the same rate as prior to the December 2019 pause. The positives during the quarter were tempered by an understandably lower than expected guidance for CYQ2 2020, due primarily to delays in purchasing by media and entertainment customers. QMCO was up 30.8% this quarter and added $0.04 to our NAV.

•Lantronix (NASDAQ:LTRX) reported record revenue for CYQ1 2020, despite supply chain and business disruptions due to the COVID-19 pandemic. LTRX saw increasing strength in the company’s remote connectivity solutions. LTRX has continued to add high-quality, former Microsemi experience to its senior leadership team (Paul Pickle, LTRX’s President/CEO was the former COO at Microsemi until its eventual takeover by Microchip). We purchased 86,269 shares at an average price per share of $3.03. LTRX was up 89.8% this quarter and added $0.07 to our NAV.

•Franchise Group (NASDAQ:FRG) is a leading North American operator and acquiror of franchised and franchisable businesses that uses its management team’s operating expertise to drive cost efficiencies and revenue synergies to grow its brands. We purchased shares of FRG in a PIPE transaction at an effective cost of $17.00 per share, which was a significant discount (~30%) to the low/mid-$20 share price at the time. FRG provided a business update in May that assuaged investor fears that the company was insolvent and/or at risk of bankruptcy. In the release, FRG estimated adjusted EPS for Q1 of $1.25 to $1.58, revenue of $585-$605 million, and cash on its balance sheet of over $120 million, which were all well above street estimates. This management team led by Brian Khan is stupendous. The company continued with its $0.25 quarterly dividend and the stock rose 160% in the quarter. We sold approximately half our position during the quarter at an average price per share of $25.80. FRG added $0.13 to our NAV in the quarter.

•Alta Equipment Group, Inc. (NYSE:ALTG) is a provider of premium materials handling equipment, construction equipment, cranes, warehouse solutions, power generation equipment, and contractors’ rental equipment. ALTG provided investors with a useful framework to understand the operating leverage in the company’s business in the face of COVID-19 related impacts. We encourage you to review their investor presentation from the prior quarter. It is a model for how companies should communicate with their investors. While business was impacted by stay-at-home orders early in the quarter, the lifting of those orders led to a quick recovery in certain markets (e.g., Florida construction-related business). ALTG also announced and closed on two acquisitions in the quarter. We purchased 104,340 shares during Q2 2020 at an average price of $4.61. ALTG stock was up 82.0% in the quarter and added $0.07 to our NAV.

Sources of material decreases in value:

•TheMaven, Inc. (OTC:MVEN) is a media coalition of professional content destinations, operating exclusively on a shared digital publishing, advertising, and distribution platform. MVEN provides a major media scale alternative to news and information on social platforms. The high-scale, unified platform offers operating leverage to all participants in MVEN’s ecosystem by eliminating all non-content operating expenses. MVEN’s distributed operating leverage enables its entire suite of services to be provided on a revenue share basis, which creates lower, non-fixed operating costs than if a media company was forced to run its own platform and digital ad sales team. MVEN provides distribution across 100+ million monthly users in a single platform, allowing advertisers to be more successful with return on investments in marketing. Among many properties, MVEN operates a 100-year license agreement to run Sports Illustrated, and it owns TheStreet.com, after purchasing that asset in 2019.

The COVID-19 pandemic shut down every sport in North America, which, in turn, caused a severe slowdown in advertising spend that has negatively impacted MVEN’s Sports Illustrated business. When you go through economic dislocation similar to what we have today, the first cost companies turn off is advertising. This economic dislocation has therefore had a severe impact on many big media companies who rely on advertising. The good news is MVEN has a significant portion of its revenues in relatively stable subscriptions revenues. MVEN has also built a tremendous platform and has seen skyrocketing views of video content. Given how widespread the weakness has been, MVEN may be in a position to take over other digital media assets from these big media companies who are looking at all ways to reduce their cost structures. However, for this stock to work, we believe major sports need to resume, the economy to stabilize, and for advertising to return to more normalized levels in the back half of the year.

MVEN is in the process of completing its financial statements so it can be up to date with all filings with the SEC. It is our expectation that after getting up to date with all filings sometime this year, MVEN will up-list to a national stock exchange. As part of our investment in the company, we are entitled to receive partial liquidating damages while the company is not up to date with its filings. As of June 30, 2020, these accrued liquidating damages are approximately $701,000, with $277,000 accrued this quarter, which partially offset the decline in the volume-weighted average price per share of MVEN’s common stock used to derive fair value. Of significant note, this quarter, 180 has joined the MVEN Board of Directors as a board observer. We currently believe, out of all the positions we own, MVEN has the chance to have the greatest return; although with that said, it carries short-term risks. MVEN is our largest publicly traded position. For the quarter, MVEN reduced our NAV by $0.05.

•Potbelly (NASDAQ:PBPB), unlike many of the holdings above, faces unique challenges through this pandemic. Stay-at-home orders have had a significant negative effect on the restaurant industry. Same store sales have plummeted throughout the industry, with full-service-only restaurants being the most impacted. Despite having zero bank debt coming into the crisis, PBPB drew its entire $40 million credit facility given the uncertain business outlook. As you know, we filed a 13D early this year noting our sizable position and intent to engage constructively with the company. Our expectation was PBPB was set to show improved results following its significant investment on a consulting project designed towards improving efficiency and comparable same store sales. If they couldn’t turn the business around, we were of the mindset that it would be time to turn the reigns over to a new team. Following the Q1 2020 earnings call, it became obvious that a change in leadership was necessary. In June 2020, we filed an amended 13D, noting the poor performance of the company under its CEO, while commending the Board for hiring a new CFO (Steve Cirulis) and two new Board members; all of whom have extensive restaurant experience. We also noted our increased ownership that makes 180 the largest reporting shareholder of PBPB. Most recently, the Board hired Robert Wright, the former COO of Wendy’s, as its new CEO. In our first encounter with Robert following the announcement of his hiring, we were more than impressed. The thing we liked the most was his decision to be paid in equity during the first year of his employment. His cash compensation for his first year is literally $1.00. Talk about an executive that understands and is fully aligned with his company’s shareholders. For the quarter, PBPB reduced our NAV by $0.04.

NEW POSITION: Sonim Technologies Inc.

Sonim Technologies Inc. (NASDAQ: SONM) is a communications company that provides rugged cellular phones and accessories specifically designed for workers who are physically engaged in their environments and often in mission-critical roles. These workers are typically in industrial/public sector enterprises operating across the construction, energy, utility, hospitality, logistics, manufacturing, public safety and transportation sectors. SONM’s business is divided into three product categories: smartphones (XP6, XP7, XP8), feature phones (XP3, XP5, XP5s), and accessories. SONM's products are generally sold to end customers by wireless carriers often on a subsidized basis. SONM generates over 90% of its revenues in the US and Canada. Primary competitors in the rugged handset market include Samsung, Kyocera, Bullitt Group Ltd. (provider of CAT branded rugged phones). Between May and September of 2019, SONM experienced technical and software issues with its devices, experienced significant carrier agreement delays, and grossly mismanaged sales delivery timing. This resulted in significantly reduced revised guidance of both the top and bottom lines and caused a decline of SONM's stock to ~$3 per share from a peak of ~$18 per share in June. SONM began restructuring efforts in September 2019 following the appointment of a new CEO (Tom Wilkinson) and CFO (Bob Tirva). Forward looking guidance was suspended as the restructuring efforts began.

In my former life following my days at Blackrock, I ran a fund called RGJ Capital where we were a significant shareholder in XPLORE Technologies (“XPLR”), which was led by Tom Wilkinson, the new CEO of SONM. Under Tom's leadership, XPLR’s business was dramatically improved and the company was ultimately acquired. 180 has confidence in Tom's abilities as an executive to engineer a similar turnaround at SONM. One of SONM’s first priorities was to clean up its balance sheet. SONM’s outstanding loans created substantial uncertainty as to the viability of the current business and prevented the company from investing in next-generation mobile devices and connectivity platforms. We believed that the removal of this debt overhang coupled with a cash infusion to fund development of future product lines could unlock value in the near term and allow management to focus on long-term value creation. This past quarter, 180 anchored a public offering of 36.8 million common shares at $0.75 per share that raised gross proceeds of $27.6 million. An additional 8.3 million shares were issued in exchange for conversion of 60% of the outstanding debt and $4 million was repaid in cash. SONM now has a clean balance sheet with no debt and substantial capital resources to fund development of its next-generation devices. 180's investment at $0.75 per share equates to an EV/TTM revenues of <0.2x. XPLR, a good comparable publicly traded company, was acquired at approximately 1x EV/TTM revenues. First responder connectivity has become increasingly important as the COVID-19 pandemic, as well as other domestic and global events, place additional importance on connectivity in all environments. This secular trend could provide meaningful growth opportunities for SONM.

Private Portfolio

For the quarter, our private portfolio increased in value by approximately $10.6 million, or $0.34 per share. The increase in value was led Petra ($0.29/share), with additional contributions from EchoPixel, Inc. ($0.03/share) and ORIG3N, Inc. ($0.03/share). These increases in value were offset in part by the decrease in Lodo Therapeutics Corporation ($0.01/share). Last quarter, a number of our private portfolio companies were adversely impacted by the COVID-19 pandemic. While many of these companies have recovered in part or in full from such impacts, it remains uncertain if negative impacts to value will return in future quarters.

We also noted that certain of our privately held companies were well positioned to provide valuable diagnostic and monitoring capabilities that could lead to material growth for those companies. For example, in April 2020, ORIG3N received an Emergency Use Authorization from the Food and Drug Administration for its novel COVID-19 diagnostic test. ORIG3N’s high-throughput automated test capabilities have generated meaningful growth for the company as it addresses this ever-increasing market need.

In last quarter’s shareholder letter we stated that, while we desire to shepherd our existing private portfolio to exits or explore opportunities to sell our positions in those companies, we have the luxury of being able to sell our private holdings when we believe it makes sense for shareholders rather than being forced to do so to survive. The remaking of our business and the significant cash and securities of publicly traded portfolio companies that we have grown mean that we don’t have to sell anything. This ability allowed us to benefit from the acquisition of Petra by an undisclosed party in Q2 2020, and possibly other liquidity events in the future.

As a refresher on the Petra acquisition, the acquiring company and the terms of the deal are confidential, so we can only speak to what 180 received from the transaction. We received approximately $4.4 million in cash at closing. In addition, we received $305,000 in cash from 180’s ownership in an entity affiliated with Petra, Accelerator IV-New York. Also, approximately $350,000 will be held in escrow for one year from the date of closing. 180 is also eligible, through its ownership in the acquired company and the affiliated entity, to receive up to approximately $86.9 million in potential future payments upon the achievement of undisclosed development and commercial milestones. 180 currently estimates that the first milestone payment could occur in 2-3 years, and subsequent milestone payments could occur at various points over the subsequent 10-20 years. The timing and likelihood of the acquirer achieving these milestones is highly uncertain, and if these milestones are achieved, the timing may be materially different than current estimates. These factors were used to develop a fair market value based on a probability-weighted net present value analysis of the potential future milestone payments of approximately $6.4 million. We note that successful completion of the first milestone alone would result in payment of approximately $6.8 million to 180. Lastly, simultaneous with the close of the transaction, Petra spun out certain assets into a new company. We own shares of this new company, Revanna Pharmaceuticals, Inc.

While we continue to believe there are other companies in the portfolio that hold promise to build value, the timelines and potential exit values for these companies are highly uncertain.

EXPENSES

As we have noted in previous letters, we have dramatically reduced our cost structure under our new strategy. In 2016, before our Fund’s change in investment focus and management team, our operating expenses, excluding stock-based compensation and interest on outstanding debt, averaged approximately $1.3 million per quarter. For Q2 2020, our operating expenses equaled approximately $893,000, a 17% increase from a year ago. A material portion of this increase was directly related to the legal expenses incurred with registering as a Registered Investment Adviser and other start-up costs associated with our new separate account for a portion of a publicly traded company’s pension fund.

TURN/NAV: SUM OF THE PARTS

As of the end of Q2 2020, TURN traded at 64.4% of its NAV. Our public securities, cash, and other assets net of liabilities were $1.40 per share. Our stock price was $1.74. If we received 100% credit for the value of these assets net of liabilities, the market is ascribing a value of approximately $0.34 per share, or approximately $10.5 million, to our private portfolio. Given our private assets are valued at approximately $40.5 million, the market is discounting the value of our private portfolio assets by 74% as of the end of Q2 2020.

As we grow our cash and liquid securities, the discount our stock trades to NAV should narrow. At the beginning of our strategy in 2017, we had 26.9% of our cash and total investments in cash and securities of public companies, and we were trading at a 41.0% discount to NAV. At the end of Q2 2020, we had 52.4% of our cash and total investments in cash and securities of public companies, and we traded at a 35.6% discount to NAV. While we have made considerable progress in changing the construct of our balance sheet, the market has barely rewarded us. There is more work to be done.

While it is aggravating to see a stock price for TURN that reflects receiving very little credit for the turnaround of our business, it is also noteworthy to comment on the lack of value attributed to our private portfolio. Petra is the most recent example that supports our belief that our stock price does not accurately reflect the value of our business. As already discussed, not only did we receive an immediate payment of $4.7 million (2x our Q1 2020 valuation), we have the ability to receive an additional $350,000 held in escrow for one year from the date of the closing of the transaction. We also retain ownership in a spinout company that will seek to monetize additional assets of the company, and we could receive future milestone payments of up to

approximately $86.9 million. We have some other biotech companies that saw their values increase this quarter due to their ability to provide needed products and services amidst the COVID-19 pandemic. AgBiome, in and of itself, has a $13.2 million value on our balance sheet and represents $0.43 of our book value. I believe the value of that position alone should allow our share price to be meaningfully above the value of our cash and public company investments, let alone others that not only have real value today, but have the potential to be monetized in the future. As always, if we don’t feel (and we absolutely do not) that we are properly being rewarded in the market for the assets we have on our balance sheet, 180’s management team will gladly head back to the open market and purchase TURN stock. As you know, I personally own approximately 900,000 shares and in total our board and management own 5.3% of 180. As you also know, because of restrictions in the Investment Company Act of 1940, we cannot pay our employees in stock. Therefore, all the stock we have bought in the open market since our inception in 2017 is with after-tax cash from our pockets.

CONCLUSION

In the middle of a global meltdown and the COVID-19 pandemic, we are proud to have received a mandate to manage a $25 million separate account for a pension fund. We started putting the money to work in early June 2020. We have talked often about exploring ways to seek capital. This announcement marks our first big win, but it won’t be our last. We will continue to build our asset base for those that want to invest in our strategy.

We live in interesting times. Not only has COVID-19 taken over our lives, real issues regarding racial injustice are dominating the day to day activities of our nation’s citizens. Add on top of all of that, we also have a presidential election in less than three months. We expect the market to experience extreme volatility as we exit the summer and into the home stretch of this calendar year. I would also note, that as of the writing of this letter (August 7, 2020), we have actually crossed from the red, with our public holdings gross total return now positive for the year; this transition is actually funny. If you took an Elon Musk shuttle around the universe for the last 8 months and four days, returned to planet Earth and saw 180 was flat for the year, you might say to yourself, “Wow, must have been a quiet year with not much happening.” Or… NOT. This has been both a wild and trying year, and I suspect we just completed the first section of this intense roller coaster. I make no assumptions that I know where this will all go, but I certainly think the meteoric rise over the last three months may have some misguided optimism regarding our ability to navigate through the COVID-19 virus pandemic. I do know this... Our quarter end book value is $2.70, and our share price starts with a “1”. Given our public portfolio gross total return is up 19.1% QTD through August 7, and our cash and securities of publicly traded companies currently equals approximately $1.70/share, I would like to think we have a long way to go to get the type of valuation our results warrant.

Thank you for your continued support.

Kevin Rendino

Chairman and Chief Executive Officer

| | |

180 DEGREE CAPITAL CORP.

CONSOLIDATED STATEMENT OF ASSETS AND LIABILITIES (UNAUDITED) |

| | | | | |

| | June 30, 2020 |

| ASSETS | |

| Investments in portfolio securities, at value: | |

| Unaffiliated privately held companies (cost: $16,371,995) | $ | 18,299,355 | |

| Unaffiliated publicly traded securities (cost: $15,145,385) | 18,195,511 | |

| Non-controlled affiliated privately held companies (cost: $34,101,772) | 14,305,640 | |

| Non-controlled affiliated publicly traded securities (cost: $23,109,373) | 17,745,078 | |

| Unaffiliated rights to payments (adjusted cost basis: $6,408,684) | 7,720,006 | |

| Cash | 7,934,245 | |

| Restricted cash | 11,639 | |

| Funds held in escrow from sales of investment, at value | 161,249 | |

| Receivable from portfolio companies and managed funds | 926,248 | |

| Prepaid expenses | 135,196 | |

| Interest receivable | 6,137 | |

| Other receivables | 71,121 | |

| Other assets | 30,319 | |

| Total assets | $ | 85,541,744 | |

| LIABILITIES & NET ASSETS | |

| |

| Post-retirement plan liabilities | $ | 1,252,460 | |

| Accounts payable and accrued liabilities | 334,041 | |

| Payable for securities purchased | 1,238 | |

| Total liabilities | $ | 1,587,739 | |

| Commitments and contingencies (Note 10) | |

| Net assets | $ | 83,954,005 | |

| Net assets are comprised of: | |

| Preferred stock, $0.10 par value, 2,000,000 shares authorized; none issued | $ | 0 | |

Common stock, $0.01 par value, 45,000,000 shares authorized; 34,623,341 issued | 334,594 | |

| Additional paid in capital | 122,785,067 | |

| Total accumulated distributable loss | (34,560,131) | |

Treasury stock, at cost 3,501,779 shares | (4,605,525) | |

| Net assets | $ | 83,954,005 | |

| Shares outstanding | 31,121,562 | |

| Net asset value per outstanding share | $ | 2.70 | |

The accompanying unaudited notes are an integral part of these unaudited consolidated financial statements.

9

| | |

180 DEGREE CAPITAL CORP.

CONSOLIDATED STATEMENT OF OPERATIONS (UNAUDITED) |

| | | | | |

| Six Months Ended

June 30, 2020 |

| Income: | |

| Interest from: | |

| Unaffiliated companies-PIK | $ | 28,685 | |

| Non-controlled affiliated companies-cash | 1,995 | |

| Non-controlled affiliated companies-PIK | 4,987 | |

| Other income (Note 2) | 595,160 | |

| Dividend income | 190,569 | |

| Fee income for providing managerial assistance to portfolio companies-non-cash | 26,895 | |

| Management fee income | 12,301 | |

| Carried interest | 4,640 | |

| Total income | 865,232 | |

| Operating fees and expenses: | |

| Salaries, bonus and benefits | 509,544 | |

| Professional | 390,492 | |

| Administration and operations | 182,473 | |

| Directors | 132,294 | |

| Insurance | 121,667 | |

| Rent | 13,674 | |

| Custody | 10,161 | |

| Other | 2,523 | |

| Total operating expenses | 1,362,828 | |

| Net investment loss before income tax expense | (497,596) | |

| Income tax expense | 122 | |

| Net investment loss | (497,718) | |

| Net realized gain (loss) from investments: | |

| Unaffiliated privately held companies | 7,963,973 | |

| Unaffiliated publicly traded securities | 1,306,521 | |

| Unaffiliated rights to payments | 23,976 | |

| Call options | (271,304) | |

| Funds held in escrow | 609 | |

| Net realized gain from investments | 9,023,775 | |

| Change in unrealized (depreciation) appreciation on investments: | |

| Unaffiliated privately held companies | (8,758,994) | |

| Unaffiliated publicly traded securities | (3,743,762) | |

| Non-controlled affiliated privately held companies | (1,758,797) | |

| Non-controlled affiliated publicly traded securities | (5,587,459) | |

| Unaffiliated rights to payments | 86,222 | |

| Net change in unrealized depreciation on investments | (19,762,790) | |

| Net realized gain from investments and change in unrealized depreciation on investments | (10,739,015) | |

| Share of loss on equity method investment | (22,901) | |

| Net decrease in net assets resulting from operations | $ | (11,259,634) | |

The accompanying unaudited notes are an integral part of these unaudited consolidated financial statements.

10

| | |

180 DEGREE CAPITAL CORP.

CONSOLIDATED STATEMENT OF CASH FLOWS (UNAUDITED) |

| | | | | |

| Six Months Ended

June 30, 2020 |

| Cash flows used in operating activities: | |

| Net decrease in net assets resulting from operations | $ | (11,259,634) | |

Adjustments to reconcile net decrease in net assets resulting from operations to net cash used in operating activities: | |

| Net realized gain from investments | (9,023,775) | |

Net change in unrealized depreciation on investments | 19,762,790 | |

| Share of loss on equity method investee | 22,901 | |

Depreciation of fixed assets | 2,523 | |

| Accretion of bridge note PIK interest income | (33,672) | |

| Fee income for providing managerial assistance to portfolio companies-non-cash | (26,895) | |

| Call options purchased | (523,562) | |

| Call options written | 252,258 | |

| Purchase of unaffiliated publicly traded securities | (11,184,359) | |

| Purchase of non-controlled affiliated publicly traded securities | (5,884,905) | |

| Distributions from sale of unaffiliated privately held companies | 4,605,796 | |

| Proceeds from sale of unaffiliated publicly traded securities | 12,803,921 | |

| Proceeds from unaffiliated rights to payments | 45,194 | |

| Changes in assets and liabilities: | |

| Increase in receivable from portfolio companies and managed funds | (681,449) | |

| Decrease in prepaid expenses | 132,757 | |

| Increase in interest receivable | (1,995) | |

| Increase in other receivables | (4,281) | |

| Decrease in other assets | 390 | |

| Decrease in receivable from sales of securities | 559,233 | |

| Decrease in post-retirement plan liabilities | (4,744) | |

| Decrease in accounts payable and accrued liabilities | (82,115) | |

| Decrease in bonus payable | (2,543,785) | |

| Decrease in payable for securities purchased | (355,375) | |

| Net cash used in operating activities | (3,422,783) | |

| Cash flows from investing activities: | |

| Purchase of fixed assets | (5,974) | |

| Net cash used in investing activities | (5,974) | |

| Net decrease in cash and restricted cash | (3,428,757) | |

| Cash and restricted cash at beginning of the period | 11,374,641 | |

| Cash and restricted cash at end of the period | $ | 7,945,884 | |

| Supplemental disclosures of cash flow information: | |

| Income taxes paid | $ | 122 | |

| |

| Cash | $ | 7,934,245 | |

| Restricted cash | 11,639 | |

| Total cash and restricted cash shown in the consolidated statement of cash flows | $ | 7,945,884 | |

The accompanying unaudited notes are an integral part of these unaudited consolidated financial statements.

11

| | |

180 DEGREE CAPITAL CORP.

CONSOLIDATED STATEMENTS OF CHANGES IN NET ASSETS |

| | | | | | | | | | | |

| Six Months Ended

June 30, 2020 | | Year Ended December 31, 2019 |

| (UNAUDITED) | | |

| Changes in net assets from operations: | | | |

| Net investment loss | $ | (497,718) | | | $ | (4,831,721) | |

| Net realized gain on investments | 9,023,775 | | | 9,642,262 | |

Net change in unrealized (depreciation) appreciation on investments | (19,762,790) | | | 8,410,882 | |

| Share of loss on equity method investment | (22,901) | | | (42,552) | |

| Net (decrease) increase in net assets resulting from operations | (11,259,634) | | | 13,178,871 | |

| Net (decrease) increase in net assets | (11,259,634) | | | 13,178,871 | |

| Net Assets: | | | |

| Beginning of the period/year | 95,213,639 | | | 82,034,768 | |

| End of the period/year | $ | 83,954,005 | | | $ | 95,213,639 | |

| | | |

The accompanying unaudited notes are an integral part of these unaudited consolidated financial statements.

12

| | |

180 DEGREE CAPITAL CORP.

CONSOLIDATED FINANCIAL HIGHLIGHTS |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Six Months Ended

June 30, 2020 | | Year Ended

Dec. 31, 2019 | | Year Ended

Dec. 31, 2018 | | Year Ended

Dec. 31, 2017 | | Year Ended

Dec. 31, 2016 | | Year Ended

Dec. 31, 2015 |

| (UNAUDITED) | | | | | | | | | | |

| Per Share Operating Performance: | | | | | | | | | | | |

| Net asset value per share, beginning of the period/year | $ | 3.06 | | | $ | 2.64 | | | $ | 2.60 | | | $ | 2.34 | | | $ | 2.88 | | | $ | 3.51 | |

Net investment loss* | (0.02) | | | (0.16) | | | (0.07) | | | (0.12) | | | (0.15) | | | (0.23) | |

Net realized gain (loss) from investments* | 0.29 | | | 0.31 | | | (0.25) | | | (0.38) | | | (0.26) | | | 0.15 | |

Net change in unrealized appreciation (depreciation) on investments and options*1 | (0.63) | | | 0.27 | | | 0.36 | | | 0.80 | | | (0.12) | | | (0.56) | |

Share of loss on equity method investment*2 | 0.00 | | | 0.00 | | | 0.00 | | | 0.00 | | | 0.00 | | | (0.01) | |

| Total* | (0.36) | | | 0.42 | | | 0.04 | | | 0.30 | | | (0.53) | | | (0.65) | |

Net (decrease) increase as a result of stock-based compensation expense*2 | 0.00 | | | 0.00 | | | 0.00 | | | (0.01) | | | 0.01 | | | 0.03 | |

Net increase as a result of purchase of treasury stock | 0.00 | | | 0.00 | | | 0.00 | | | 0.00 | | | 0.00 | | | 0.01 | |

Net decrease as a result of acquisition of vested restricted stock awards related to employee withholding2 | 0.00 | | | 0.00 | | | 0.00 | | | (0.02) | | | (0.01) | | | (0.01) | |

| Total (decrease) increase from capital stock transactions | 0.00 | | | 0.00 | | | 0.00 | | | (0.03) | | | 0.00 | | | 0.03 | |

Net (decrease) increase as a result of other comprehensive (loss) income*2 | 0.00 | | | 0.00 | | | 0.00 | | | (0.01) | | | (0.01) | | | (0.01) | |

| Net increase (decrease) in net asset value | (0.36) | | | 0.42 | | | 0.04 | | | 0.26 | | | (0.54) | | | (0.63) | |

| Net asset value per share, end of the period/year | $ | 2.70 | | | $ | 3.06 | | | $ | 2.64 | | | $ | 2.60 | | | $ | 2.34 | | | $ | 2.88 | |

| Stock price per share, end of the period/year | $ | 1.74 | | | $ | 2.15 | | | $ | 1.75 | | | $ | 1.97 | | | $ | 1.38 | | | $ | 2.20 | |

| Total return based on stock price | (19.07) | % | | 22.86 | % | | (11.17) | % | | 42.75 | % | | (37.27) | % | | (25.42) | % |

| Supplemental Data: | | | | | | | | | | | |

| Net assets, end of the period/year | $ | 83,954,005 | | | $ | 95,213,639 | | | $ | 82,034,768 | | | $ | 81,042,989 | | | $ | 72,255,610 | | | $ | 88,711,671 | |

Ratio of expenses, excluding taxes, to quarterly average net assets | 1.67 | % | 3 | 6.42 | % | ^ | 3.62 | % | ^ | 6.26 | % | ^ | 7.88 | % | | 8.15 | % |

Ratio of expenses, including taxes, to quarterly average net assets | 1.67 | % | 3 | 6.42 | % | ^ | 3.63 | % | ^ | 6.28 | % | 4^ | 7.89 | % | | 8.15 | % |

Ratio of net investment loss to quarterly average net assets | (0.61) | % | 3 | (5.42) | % | | (2.82) | % | | (4.68) | % | | (5.64) | % | | (7.22) | % |

| Average debt outstanding | $ | 0 | | | $ | 0 | | | $ | 0 | | | $ | 0 | | | $ | 4,590,164 | | | $ | 3,780,822 | |

| Average debt per share | $ | 0.00 | | | $ | 0.00 | | | $ | 0.00 | | | $ | 0.00 | | | $ | 0.15 | | | $ | 0.12 | |

| Portfolio turnover | 22.61 | % | | 30.17 | % | | 20.43 | % | | 8.83 | % | | ** | | ** |

Number of shares outstanding, end of the period/year | 31,121,562 | | | 31,121,562 | | | 31,121,562 | | | 31,121,562 | | | 30,904,209 | | | 30,845,754 | |

*Based on average shares outstanding.

^ The Company has entered into an expense offsetting arrangement with one of its unaffiliated brokers relating to broker fees paid. The total broker fee charged to the Company was applied as a credit to fees charged by an affiliate of the unaffiliated broker who the Company subscribes to for data services billed during the period/year. The Company received an offset to expense totaling approximately $15,700, $17,500 and $5,700 with that broker for the years ended December 31, 2019, December 31, 2018 and December 31, 2017, respectively. The Company received an offset to expense totaling approximately $11,300 with that broker for the period ended June 30, 2020.

**Prior to March 2017, the Company was a business development company investing primarily in privately held securities. Portfolio turnover was not a relevant indicator for such investments given that the Company did not generally pay brokerage fees on such investments.

1 Net unrealized losses include rounding adjustments to reconcile change in net asset value per share.

2 Amounts listed as zero are amounts calculated as less than $0.005.

3 Not annualized.

4 Ratio of expenses, including taxes and excluding expenses related to restructuring, to quarterly average net assets for the year ended December 31, 2017 was 5.19%.

The accompanying unaudited notes are an integral part of these unaudited consolidated financial statements.

13

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| 180 DEGREE CAPITAL CORP. CONSOLIDATED SCHEDULE OF INVESTMENTS AS OF JUNE 30, 2020 (UNAUDITED) | | | | | | | | | |

| | | | | | | | | |

| Method of

Valuation (1) | | Industry | | Shares/Principal | | Cost | | Value |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Investments in Unaffiliated Companies (2) - | | | | | | | | | |

| 43.5% of net assets at value | | | | | | | | | |

| | | | | | | | | |

| Privately Held Companies (Illiquid) - | | | | | | | | | |

| 21.8% of net assets at value | | | | | | | | | |

| | | | | | | | | |

| AgBiome, LLC (3)(4) | | | Fertilizers & Agricultural Chemicals | | | | | | |

| Develops agricultural products that reduce risk and improve yield | | | | | | | | | |

| Series A-1 Convertible Preferred Units (acquired 1/30/13) | (I) (L3) | | | | 2,000,000 | | | $ | 2,000,000 | | | $ | 10,144,876 | |

| Series A-2 Convertible Preferred Units (acquired 4/9/13-10/15/13) | (I) (L3) | | | | 417,392 | | | 521,740 | | | 2,154,611 | |

| Series B Convertible Preferred Units (acquired 8/7/15) | (I) (L3) | | | | 160,526 | | | 500,006 | | | 935,987 | |

| | | | | | | 3,021,746 | | | 13,235,474 | |

| | | | | | | | | |

| AutoTech Ventures Management I, LLC (3)(4)(5) | | | Asset Management & Custody Banks | | | | | | |

| Venture capital investing in automotive-related companies | | | | | | | | | |

| LLC Interests (acquired 12/1/17) | (M) (L3) | | | | 0 | | | 0 | | | 125,000 | |

| | | | | | | | | |

| DWSI Holdings, Inc. (3)(4)(6) | | | Technology Hardware, Storage & Peripherals | | | | | | |

| Develops high-performance quantum computing systems | | | | | | | | | |

| Class A Convertible Preferred Stock (acquired 4/14/20) | (I) (L3) | | | | 1,025,046 | | | 5,662,954 | | | 1,235,956 | |

| | | | | | | | | |

| Fleet Health Alliance, LLC (3)(4) | | | Health Care Technology | | | | | | |

| Develops software for information transfer amongst healthcare providers and consumers | | | | | | | | | |

| Unsecured Convertible Bridge Note, 0%, (acquired 4/22/16, no maturity date) | (I) (L3) | | | | $ | 225,000 | | | 225,000 | | | 0 | |

| | | | | | | | | |

| Lodo Therapeutics Corporation (3) | | | Pharmaceuticals | | | | | | |

| Develops novel therapeutics derived from a metagenome-based Natural Product Discovery Platform | | | | | | | | | |

| Series A Convertible Preferred Stock (acquired 12/21/15-4/22/16) | (I) (L3) | | | | 658,190 | | | 658,190 | | | 353,601 | |

| Secured Convertible Bridge Note, 6% PIK, (acquired 6/27/19, maturing 5/7/21) | (M) (L3) | | | | $ | 474,019 | | | 502,850 | | | 502,850 | |

| | | | | | | 1,161,040 | | | 856,451 | |

| | | | | | | | | |

The accompanying unaudited notes are an integral part of this unaudited consolidated financial statements.

14

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| 180 DEGREE CAPITAL CORP. CONSOLIDATED SCHEDULE OF INVESTMENTS AS OF JUNE 30, 2020 (UNAUDITED) | | | | | | | | | |

| | | | | | | | | |

| Method of

Valuation (1) | | Industry | | Shares/Principal | | Cost | | Value |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Investments in Unaffiliated Companies (2) - | | | | | | | | | |

| 43.5% of net assets at value (cont.) | | | | | | | | | |

| | | | | | | | | |

| Privately Held Companies (Illiquid) - | | | | | | | | | |

| 21.8% of net assets at value (cont.) | | | | | | | | | |

| | | | | | | | | |

| Magnolia Neurosciences Corporation (3)(4) | | | Pharmaceuticals | | | | | | |

| Develops novel therapeutics for treatment of neurodegeneration | | | | | | | | | |

| Series A Convertible Preferred Stock (acquired 8/3/18) | (I) (L3) | | | | 862,872 | | | $ | 862,872 | | | $ | 655,897 | |

| | | | | | | | | |

| Nanosys, Inc. (3)(4) | | | Specialty Chemicals | | | | | | |

| Develops inorganic nanowires and quantum dots for use in LED-backlit devices | | | | | | | | | |

| Series C Convertible Preferred Stock (acquired 4/10/03) | (I) (L3) | | | | 803,428 | | | 1,500,000 | | | 440,676 | |

| Series D Convertible Preferred Stock (acquired 11/7/05) | (I) (L3) | | | | 1,016,950 | | | 3,000,003 | | | 895,344 | |

| Series E Convertible Preferred Stock (acquired 8/13/10) | (I) (L3) | | | | 433,688 | | | 496,573 | | | 470,149 | |

| | | | | | | 4,996,576 | | | 1,806,169 | |

| | | | | | | | | |

| NanoTerra, Inc. (3)(4) | | | Research & Consulting Services | | | | | | |

| Develops surface chemistry and nano-manufacturing solutions | | | | | | | | | |

| Warrants for Common Stock expiring on 2/22/21 (acquired 2/22/11) | (I) (L3) | | | | 4,462 | | | 69,168 | | | 0 | |

| Warrants for Series A-3 Preferred Stock expiring on 11/15/22 (acquired 11/15/12) | (I) (L3) | | | | 47,508 | | | 35,403 | | | 0 | |

| | | | | | | 104,571 | | | 0 | |

| | | | | | | | | |

| Revanna Pharmaceuticals, Inc. (3)(4)(7)(8) | | | Pharmaceuticals | | | | | | |

| Holding company for intellectual property in oncology therapeutics | | | | | | | | | |

| Common Stock (acquired 5/14/20) | (M) (L3) | | | | 2,584,763 | | | 103,391 | | | 103,391 | |

| | | | | | | | | |

| Phylagen, Inc. (3)(4) | | | Research & Consulting Services | | | | | | |

| Develops technology to improve human health and business productivity | | | | | | | | | |

| Series A Convertible Preferred Stock (acquired 11/14/18) | (M) (L3) | | | | 548,031 | | | 233,845 | | | 281,017 | |

| | | | | | | | | |

| Total Unaffiliated Privately Held Companies (cost: $16,371,995) | | | | | | | | | $ | 18,299,355 | |

| | | | | | | | | |

The accompanying unaudited notes are an integral part of this unaudited consolidated financial statements.

15

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| 180 DEGREE CAPITAL CORP. CONSOLIDATED SCHEDULE OF INVESTMENTS AS OF JUNE 30, 2020 (UNAUDITED) | | | | | | | | | |

| | | | | | | | | |

| Method of

Valuation (1) | | Industry | | Shares/Principal | | Cost | | Value |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Investments in Unaffiliated Companies (2) - | | | | | | | | | |

| 43.5% of net assets at value (cont.) | | | | | | | | | |

| | | | | | | | | |

| Unaffiliated Publicly Traded Securities - | | | | | | | | | |

| 21.7% of net assets at value | | | | | | | | | |

| | | | | | | | | |

| Alta Equipment Group, Inc. (4) | | | Trading Companies & Distributors | | | | | | |

| Operates as an industrial and construction equipment company | | | | | | | | | |

| Common Stock (Unrestricted) (acquired 2/14/20-5/15/20) | (M) (L1) | | | | 558,628 | | | $ | 4,388,085 | | | $ | 4,340,540 | |

| Warrants for the Purchase of Common Stock expiring 4/8/24 (acquired 2/14/20) | (M) (L1) | | | | 150,000 | | | 222,879 | | | 157,095 | |

| | | | | | | 4,610,964 | | | 4,497,635 | |

| | | | | | | | | |

| Franchise Group, Inc. | | | Specialized Consumer Services | | | | | | |

| Operates franchised and franchisable businesses | | | | | | | | | |

| Common Stock (acquired 3/12/20) | (M) (L1) | | | | 143,169 | | | 2,433,874 | | | 3,132,538 | |

| | | | | | | | | |

| Lantronix, Inc. (4) | | | Communications Equipment | | | | | | |

| Provides secure data access and management solutions | | | | | | | | | |

| Common Stock (acquired 9/18/18-6/24/20) | (M) (L1) | | | | 1,215,671 | | | 3,882,559 | | | 4,510,139 | |

| | | | | | | | | |

| OpGen, Inc. (4)(9) | | | Biotechnology | | | | | | |

| Developing tools for genomic sequence assembly and analysis | | | | | | | | | |

| Warrants for the Purchase of Common Stock expiring 2/17/25 (acquired 5/5/15) | (I) (L3) | | | | 62 | | | 785 | | | 27 | |

| | | | | | | | | |

| Quantum Corporation (4) | | | Technology Hardware, Storage & Peripherals | | | | | | |

| Provides high-density data storage and high-speed data processing solutions | | | | | | | | | |

| Common Stock (acquired 2/4/19-4/7/20) | (M) (L1) | | | | 1,515,605 | | | 4,022,813 | | | 5,850,235 | |

| | | | | | | | | |

| Miscellaneous Common Stocks (10) | (M) (L1) | | | | | | 194,390 | | | 204,937 | |

| | | | | | | | | |

| Total Unaffiliated Publicly Traded Securities (cost: $15,145,385) | | | | | | | | | $ | 18,195,511 | |

| | | | | | | | | |

| Total Investments in Unaffiliated Companies (cost: $31,517,380) | | | | | | | | | $ | 36,494,866 | |

| | | | | | | | | |

The accompanying unaudited notes are an integral part of this unaudited consolidated financial statements.

16

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| 180 DEGREE CAPITAL CORP. CONSOLIDATED SCHEDULE OF INVESTMENTS AS OF JUNE 30, 2020 (UNAUDITED) | | | | | | | | | |

| | | | | | | | | |

| Method of

Valuation (1) | | Industry | | Shares/Principal | | Cost | | Value |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Investments in Non-Controlled Affiliated Companies (2) - | | | | | | | | | |

| 38.2% of net assets at value | | | | | | | | | |

| | | | | | | | | |

| Privately Held Companies (Illiquid) - | | | | | | | | | |

| 17.0% of net assets at value | | | | | | | | | |

| | | | | | | | | |

| ABSMaterials, Inc. (3) | | | Specialty Chemicals | | | | | | |

| Develops nano-structured absorbent materials for water remediation and consumer applications | | | | | | | | | |

| Series A Convertible Preferred Stock (acquired 2/17/10-10/24/11) | (I) (L3) | | | | 390,000 | | | $ | 435,000 | | | $ | 23,064 | |

| Series B Convertible Preferred Stock (acquired 11/8/13-6/25/14) | (I) (L3) | | | | 1,037,751 | | | 1,217,644 | | | 319,984 | |

| Secured Convertible Bridge Note, 8% PIK, (acquired 1/20/16, maturing 12/31/20) | (M) (L3) | | | | $ | 100,000 | | | 135,595 | | | 135,595 | |

| Secured Convertible Bridge Note, 8% PIK, (acquired 3/28/17, maturing 12/31/20) | (M) (L3) | | | | $ | 25,000 | | | 31,526 | | | 31,526 | |

| | | | | | | 1,819,765 | | | 510,169 | |

| | | | | | | | | |

| Accelerator IV-New York Corporation (3)(11) | | | Research & Consulting Services | | | | | | |

| Identifies and managing emerging biotechnology companies | | | | | | | | | |

| Series A Common Stock (acquired 7/21/14-12/12/18) | (I) (L3) | | | | 833,333 | | 0 | | 679,446 | |

| | | | | | | | | |

| Black Silicon Holdings, Inc. (3)(4)(8)(12) | | | Semiconductors | | | | | | |

| Holding company for interest in a company that develops silicon-based optoelectronic products | | | | | | | | | |

| Series A Convertible Preferred Stock (acquired 8/4/15) | (M) (L3) | | | | 233,499 | | | 750,000 | | | 0 | |

| Series A-1 Convertible Preferred Stock (acquired 8/4/15) | (M) (L3) | | | | 2,966,667 | | | 890,000 | | | 0 | |

| Series A-2 Convertible Preferred Stock (acquired 8/4/15) | (M) (L3) | | | | 4,207,537 | | | 2,445,000 | | | 0 | |

| Series B-1 Convertible Preferred Stock (acquired 8/4/15) | (M) (L3) | | | | 1,892,836 | | | 1,169,561 | | | 0 | |

| Series C Convertible Preferred Stock (acquired 8/4/15) | (M) (L3) | | | | 1,674,030 | | | 1,171,316 | | | 0 | |

| Secured Convertible Bridge Note, 8% PIK, (acquired 8/25/16, maturing 8/4/21) | (M) (L3) | | | | $ | 1,278,453 | | | 1,444,368 | | | 263,994 | |

| | | | | | | 7,870,245 | | | 263,994 | |

| | | | | | | | | |

The accompanying unaudited notes are an integral part of this unaudited consolidated financial statements.

17

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| 180 DEGREE CAPITAL CORP. CONSOLIDATED SCHEDULE OF INVESTMENTS AS OF JUNE 30, 2020 (UNAUDITED) | | | | | | | | | |

| | | | | | | | | |

| Method of

Valuation (1) | | Industry | | Shares/Principal | | Cost | | Value |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Investments in Non-Controlled Affiliated Companies (2) - | | | | | | | | | |

| 38.2% of net assets at value (cont.) | | | | | | | | | |

| | | | | | | | | |

| Privately Held Companies (Illiquid) - | | | | | | | | | |

| 17.0% of net assets at value (cont.) | | | | | | | | | |

| | | | | | | | | |

| EchoPixel, Inc. (3)(4) | | | Health Care Equipment | | | | | | |

| Develops virtual reality 3-D visualization software for life sciences and health care applications | | | | | | | | | |

| Series Seed Convertible Preferred Stock (acquired 6/21/13-6/30/14) | (I) (L3) | | | | 4,194,630 | | | $ | 1,250,000 | | | $ | 1,010,296 | |

| Series Seed-2 Convertible Preferred Stock (acquired 1/22/16) | (I) (L3) | | | | 1,476,668 | | | 500,000 | | | 360,137 | |

| Series A-2 Convertible Preferred Stock (acquired 3/23/17) | (I) (L3) | | | | 1,471,577 | | | 350,000 | | | 424,659 | |

| | | | | | | 2,100,000 | | | 1,795,092 | |

| | | | | | | | | |

| Essential Health Solutions, Inc. (3) | | | Health Care Technology | | | | | | |

| Develops software for information transfer amongst healthcare providers and consumers | | | | | | | | | |

| Common Stock (acquired 11/18/16) | (I) (L3) | | | | 200,000 | | | 20 | | | 132,476 | |

| Series A Convertible Preferred Stock (acquired 11/18/16) | (I) (L3) | | | | 2,750,000 | | | 2,750,000 | | | 2,677,951 | |

| Unsecured Convertible Bridge Note, 8%, (acquired 12/19/18, maturing 12/19/21) | (I) (L3) | | | | $ | 50,000 | | | 50,000 | | | 50,000 | |

| | | | | | | 2,800,020 | | | 2,860,427 | |

| | | | | | | | | |

| HALE.life Corporation (3)(4) | | | Health Care Technology | | | | | | |

| Develops a platform to facilitate precision health and medicine | | | | | | | | | |

| Common Stock (acquired 3/1/16) | (I) (L3) | | | | 1,000,000 | | | 10 | | | 68,198 | |

| Series Seed-1 Convertible Preferred Stock (acquired 3/28/17) | (I) (L3) | | | | 11,000,000 | | | 1,896,920 | | | 1,096,668 | |

| Series Seed-2 Convertible Preferred Stock (acquired 12/28/18) | (I) (L3) | | | | 12,083,132 | | | 2,500,000 | | | 1,287,815 | |

| | | | | | | 4,396,930 | | | 2,452,681 | |

| | | | | | | | | |

| ORIG3N, Inc. (3)(4) | | | Health Care Technology | | | | | | |

| Develops consumer focused genetic tests | | | | | | | | | |

| Series 1 Convertible Preferred Stock (acquired 2/5/15-8/5/15) | (H) (L3) | | | | 1,195,315 | | | 500,000 | | | 1,140,952 | |

| Series A Convertible Preferred Stock (acquired 11/25/15-9/7/16) | (H) (L3) | | | | 1,364,666 | | | 1,500,000 | | | 1,357,551 | |

| Series A-2 Convertible Preferred Stock (acquired 5/11/17-2/8/18) | (H) (L3) | | | | 176,386 | | | 200,002 | | | 185,280 | |

| | | | | | | 2,200,002 | | | 2,683,783 | |

| | | | | | | | | |

The accompanying unaudited notes are an integral part of this unaudited consolidated financial statements.

18

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| 180 DEGREE CAPITAL CORP. CONSOLIDATED SCHEDULE OF INVESTMENTS AS OF JUNE 30, 2020 (UNAUDITED) | | | | | | | | | |

| | | | | | | | | |

| Method of

Valuation (1) | | Industry | | Shares/Principal | | Cost | | Value |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Investments in Non-Controlled Affiliated Companies (2) - | | | | | | | | | |

| 38.2% of net assets at value (cont.) | | | | | | | | | |

| | | | | | | | | |

| Privately Held Companies (Illiquid) - | | | | | | | | | |

| 17.0% of net assets at value (cont.) | | | | | | | | | |

| | | | | | | | | |

| Produced Water Absorbents, Inc. (3)(4)(13)(14) | | | Oil & Gas Equipment & Services | | | | | | |

| Provides integrated process separation solutions to the global oil and gas industries, enabling onsite treatment of produced and flowback water | | | | | | | | | |

| Common Stock (acquired 4/30/16) | (M) (L3) | | | | 50,243,350 | | | $ | 7,670,281 | | | $ | 0 | |

| Warrants for Common Stock expiring upon liquidation event (acquired 4/30/16) | (M) (L3) | | | | 450,000 | | | 65,250 | | | 0 | |

| Senior Secured Debt, 15% commencing on 4/1/16, matured on 12/31/19 (acquired 4/1/16) | (M) (L3) | | | | $ | 2,533,766 | | | 2,533,766 | | | 0 | |

| | | | | | | 10,269,297 | | | 0 | |

| | | | | | | | | |

| TARA Biosystems, Inc. (3)(4) | | | Life Sciences Tools & Services | | | | | | |

| Develops human tissue models for toxicology and drug discovery applications | | | | | | | | | |

| Common Stock (acquired 8/20/14) | (I) (L3) | | | | 2,000,000 | | | 20 | | | 543,932 | |

| Series A Convertible Preferred Stock (acquired 3/31/17) | (I) (L3) | | | | 6,878,572 | | | 2,545,493 | | | 2,438,255 | |

| Series A-2 Convertible Preferred Stock (acquired 4/18/19) | (I) (L3) | | | | 208,577 | | | 100,000 | | | 77,861 | |

| | | | | | | 2,645,513 | | | 3,060,048 | |

| | | | | | | | | |

| Total Non-Controlled Affiliated Privately Held Companies (cost: $34,101,772) | | | | | | | | | $ | 14,305,640 | |

| | | | | | | | | |

| Non-Controlled Affiliated Publicly Traded Securities - | | | | | | | | | |

| 21.2% of net assets at value | | | | | | | | | |

| | | | | | | | | |

| Potbelly Corporation (4) | | | Restaurants | | | | | | |

| Operates a chain of sandwich shops | | | | | | | | | |

| Common Stock (acquired 6/24/19-6/1/20) | (M) (L1) | | | | 1,489,455 | | | $ | 6,195,900 | | | $ | 3,395,957 | |

| | | | | | | | | |

| Sonim Technologies, Inc. (4) | | | Technology Hardware, Storage & Peripherals | | | | | | |

| Provides rugged communications products | | | | | | | | | |

| Common Stock (acquired 6/5/20-6/30/20) | (M) (L1) | | | | 5,901,547 | | | 4,426,238 | | | 4,726,549 | |

| | | | | | | | | |

The accompanying unaudited notes are an integral part of this unaudited consolidated financial statements.

19

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| 180 DEGREE CAPITAL CORP. CONSOLIDATED SCHEDULE OF INVESTMENTS AS OF JUNE 30, 2020 (UNAUDITED) | | | | | | | | | |

| | | | | | | | | |

| Method of

Valuation (1) | | Industry | | Shares/Principal | | Cost | | Value |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Investments in Non-Controlled Affiliated Companies (2) - | | | | | | | | | |

| 38.2% of net assets at value (cont.) | | | | | | | | | |

| | | | | | | | | |

| Non-Controlled Affiliated Publicly Traded Securities - | | | | | | | | | |

| 21.2% of net assets at value (cont.) | | | | | | | | | |

| | | | | | | | | |

| Synacor, Inc. (4)(15) | | | Application Software | | | | | | |

| Provides technology development, multiplatform services and revenue partner for video, internet and communications providers, device manufacturers, and enterprises | | | | | | | | | |

| Common Stock (acquired 4/6/17-4/1/20) | (M) (L1) | | | | 1,720,888 | | | $ | 4,487,235 | | | $ | 1,944,603 | |

| Stock Options for Common Stock Expiring 2/28/29 (acquired 3/1/19) (3)(16) | (I) (L3) | | | | 50,000 | | | 0 | | | 24,607 | |

| Stock Options for Common Stock Expiring 5/16/29 (acquired 5/16/19) (3)(16) | (I) (L3) | | | | 15,000 | | | 0 | | | 7,692 | |

| Restricted Stock Units (acquired 2/27/20) (3)(16) | (M) (L2) | | | | 10,072 | | | 0 | | | 11,381 | |

| | | | | | | 4,487,235 | | | 1,988,283 | |

| | | | | | | | | |

| TheMaven, Inc. (3)(4) | | | Interactive Media & Services | | | | | | |

| Provides a shared digital publishing, advertising and distribution platform | | | | | | | | | |

| Series H Convertible Preferred Stock (acquired 6/27/19) | (M) (L2) | | | | 1,320 | | | 2,000,000 | | | 1,981,916 | |

| Series I Convertible Preferred Stock (acquired 6/28/19) | (M) (L2) | | | | 5,000 | | | 5,000,000 | | | 4,954,246 | |

| Series J Convertible Preferred Stock (acquired 10/7/19) | (M) (L2) | | | | 1,000 | | | 1,000,000 | | | 698,127 | |

| | | | | | | 8,000,000 | | | 7,634,289 | |

| | | | | | | | | |

| Total Non-Controlled Affiliated Publicly Traded Securities (cost: $23,109,373) | | | | | | | | | $ | 17,745,078 | |

| | | | | | | | | |

| Total Investments in Non-Controlled Affiliated Companies (cost: $57,211,145) | | | | | | | | | $ | 32,050,718 | |

| | | | | | | | | |

| Total Investments (cost: $88,728,525) | | | | | | | | | $ | 68,545,584 | |

| | | | | | | | | |

| | | | | | | | | |

The accompanying unaudited notes are an integral part of this unaudited consolidated financial statements.

20

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| 180 DEGREE CAPITAL CORP. CONSOLIDATED SCHEDULE OF INVESTMENTS AS OF JUNE 30, 2020 (UNAUDITED) | | | | | | | | | |

| | | | | | | | | |

| Method of

Valuation (1) | | Industry | | Shares/Principal | | Cost | | Value |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Other Financial Instruments (17) | | | | | | | | | |

| | | | | | | | | |

| Unaffiliated Rights to Payments (Illiquid) - | | | | | | | | | |

| 9.2% of net assets at value | | | | | | | | | |

| | | | | | | | | |

| Rights to Milestone Payments from Acquisition of BioVex Group, Inc. (acquired 3/4/11) (3)(4)(18) | (I) (L3) | | Biotechnology | | $ | 548,998 | | | $ | 548,998 | | | $ | 1,816,050 | |

| | | | | | | | | |

| Rights to Milestone Payments from Acquisition of Petra Pharma Corporation (acquired 5/14/20) (3)(4)(19) | (I) (L3) | | Pharmaceuticals | | $ | 5,859,686 | | | 5,859,686 | | | 5,903,956 | |

| | | | | | | | | |

| Rights to Payments from the Merger with Xenio Systems, Inc. (acquired 10/20/17) (3)(4)(20) | (I) (L3) | | Technology Hardware, Storage & Peripherals | | $ | 0 | | | 0 | | 0 | |

| | | | | | | | | |

| Total Unaffiliated Rights to Payments (adjusted cost: $6,408,684) | | | | | | | | | $ | 7,720,006 | |

| | | | | | | | | |

| Total Investments in Privately Held Companies and Publicly Traded Securities and Other Financial Instruments (cost: $95,137,209) | | | | | | | | | $ | 76,265,590 | |

The accompanying unaudited notes are an integral part of this unaudited consolidated financial statements.

21

180 DEGREE CAPITAL CORP.

NOTES TO CONSOLIDATED SCHEDULE OF INVESTMENTS AS OF JUNE 30, 2020

(UNAUDITED)

Notes to Consolidated Schedule of Investments

(1)See Note 2. Summary of Significant Accounting Policies of the Notes to Consolidated Financial Statements (Unaudited).

(2)Investments in unaffiliated companies consist of investments in which we own less than five percent of the voting shares of the portfolio company. Investments in non-controlled affiliated companies consist of investments in which we own five percent or more, but less than 25 percent, of the voting shares of the portfolio company, or where we control one or more seats on the portfolio company’s board of directors but do not control the company. Investments in controlled affiliated companies consist of investments in which we own 25 percent or more of the outstanding voting rights of the portfolio company or otherwise control the company, including control of a majority of the seats on the board of directors, or more than 25 percent of the seats on the board of directors, with no other entity or person in control of more director seats than us.

(3)We are subject to legal restrictions on the sale of all or a portion of our investment(s) in this company. The total amount of restricted securities held is $48,002,970, or 57.2 percent of net assets.

(4)Represents a non-income producing investment. Investments that have not paid dividends or interest within the last 12 months or are on non-accrual status for at least 12 consecutive months are considered to be non-income producing.

(5)We received LLC Interests of 1.25 percent in AutoTech Ventures Management I, LLC ("AutoTech") pursuant to an Administrative Services Agreement between us and AutoTech and due to us following the termination of a former employee of the Company. These LLC Interests were separate from the compensation received for providing the administrative services under the agreement that were paid in cash. The LLC interests have a capital percentage of 0 percent.

(6)The Company initially invested in D-Wave Systems, Inc. starting in 2008 and through 2014, acquiring various classes of preferred stock. On April 14, 2020, D-Wave Systems, Inc. reorganized as a subsidiary of a new company, DWSI Holdings, Inc. ("DWSI"). As part of the reorganization, all of the outstanding stock of D-Wave Systems, Inc., was consolidated into a single class of preferred stock of DWSI on a one-for-one basis. DWSI then completed a 1-for-5 reverse stock split. DWSI continues to do business as D-Wave Systems, Inc. and is located and doing business primarily in Canada. We invested in D-Wave Systems, Inc. and now DWSI, through Parallel Universes, Inc., a Delaware company.

(7)The Company received shares of Revanna Pharmaceuticals, Inc., as part of the consideration of the acquisition of Petra Pharma Corporation.

(8)Represents a non-operating entity that exists to collect future payments from licenses or other engagements, monetize assets for future distributions to investors and debt holders, or is in the process of shutting down and distributing remaining assets according to a liquidation waterfall.

(9)On August 28, 2019, OpGen, Inc. effectuated a 1:20 reverse stock split of its common stock. The warrants held by the Company are for the purchase of common stock.

(10)The identities of these securities have been concealed to protect the Company while it completes a purchase or selling program for these securities.

(11)Historically, Accelerator IV-New York Corporation ("Accelerator") was valued under the equity method of accounting. In May 2020, the Company received distributions of its pro rata share of the distribution Accelerator received from the acquisition of Petra Pharma Corporation. The Company could receive further distributions as is described in more detail in Note 2. Summary of Significant Accounting Policies. As a result of this transaction, Accelerator is fair valued by the Company's Board of Directors, under the income approach.

The accompanying unaudited notes are an integral part of this unaudited consolidated financial statements.

22

180 DEGREE CAPITAL CORP.

NOTES TO CONSOLIDATED SCHEDULE OF INVESTMENTS AS OF JUNE 30, 2020

(UNAUDITED)

(12)On August 4, 2015, SiOnyx, Inc., reorganized its corporate structure to become a subsidiary of a new company, Black Silicon Holdings, Inc. Our security holdings of SiOnyx, Inc. were converted into securities of Black Silicon Holdings, Inc. SiOnyx, Inc. was then acquired by an undisclosed buyer. Black Silicon Holdings, Inc. owns a profit interest in the undisclosed buyer.

(13)Produced Water Absorbents, Inc., also does business as ProSep, Inc.

(14)The Company's senior secured debt security of Produced Water Absorbents, Inc., matured on December 31, 2019, but was not repaid. The Company has agreed to extend the maturity date of the secured debt security and an agreement is in process. The repayment of the debt is uncertain.

(15)The Company is the Investment Manager and Managing Member of 180.2 SPV Series - a Series of 180 Degree Capital Management, LLC that owns 1,241,400 shares, or 3.2 percent of the voting securities, of Synacor, Inc. ("SYNC"). When combined with the Company's ownership of 4.4 percent of the voting securities of SYNC, the Company controls 7.6 percent of the voting securities of SYNC, based on 39,449,337 shares reported in SYNC's most recent Securities and Exchange Commission ("SEC") filing, Form 10-Q, as of March 31, 2020.

(16)The stock options and restricted stock units were issued to Kevin Rendino for service on the Board of Directors of SYNC. Mr. Rendino entered into an assignment and assumption agreement with the Company that transfers all beneficial and voting interest to the Company.

(17)Other financial instruments are holdings of the Company that do not meet the definition of a security or a derivative.

(18)If all the remaining milestones are met, we would receive $5,384,482. There can be no assurance as to how much of these amounts we will ultimately realize or when they will be realized, if at all.

(19)If all the remaining milestones are met, we would receive $80,603,393. There can be no assurance as to how much of these amounts we will ultimately realize or when they will be realized, if at all.

(20)In October 2017, Xenio Systems, Inc., merged with Xenio Holdings, Inc. In conjunction with this merger, all common stock of Xenio Systems, Inc., was canceled and shareholders were granted a right to a future payment in the event of a sale of Xenio Holdings, Inc. The maximum amount we could receive from such payments is approximately $11,100. There can be no assurance as to how much of these amounts we will ultimately realize or when they will be realized, if at all.

The accompanying unaudited notes are an integral part of this unaudited consolidated financial statements.

23

180 DEGREE CAPITAL CORP.

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

(UNAUDITED)

NOTE 1. THE COMPANY