UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANY

Investment Company Act file number 811-07074

| | |

| 180 DEGREE CAPITAL CORP. |

| (Exact Name of Registrant as Specified in Its Charter) |

| | | | | | | | |

| 7 N. Willow Street, Suite 4B, Montclair NJ | | 07042 |

| (Address of Principal Executive Offices) | | (Zip Code) |

| | |

Daniel B. Wolfe

President and Chief Financial Officer

180 Degree Capital Corp.

7 N. Willow Street, Suite 4B

Montclair, NJ 07042 |

| (Name and address of agent for service) |

|

Copy to:

John J. Mahon, Esq.

Proskauer Rose, LLP

1001 Pennsylvania Avenue, NW

Suite 600 South

Washington, DC 20004-2533

(202) 416-6828 |

Registrant's telephone number, including area code: (973) 746-4500

Date of fiscal year end: December 31

Date of reporting period: June 30, 2023

Item 1. Report to Shareholders.

Fellow Shareholders,

This is my 26th shareholder letter since the start of 180 in 2017. I feel like I'm running out of creative things to write about or funny stories to tell. I don’t even know what to say at this point that is riveting or thought provoking. I am even running out of sports analogies. We have been transparent about our strategy and outward in describing what we own and why. It’s truly a rinse repeat situation this quarter, similar to many of the quarters over the past 18 months. We own what we own, and we believe there is enormous value in what we own. We currently expect to be paid in an exceptionally large way over the next few years as that value is recognized by the public markets. I'm just exhausted from saying that aloud at this point.

So many people think they are irreplaceable. There are very few that are. I am not one of them, nor have I ever thought I was. When I left BlackRock in 2012, I was 100% convinced that they would find someone to replace me, and the world would not end. To that end, and following my comments above, I have determined even my authorship of shareholder letters could be replaced by today’s artificial intelligence systems. Let’s therefore experiment with ChatGPT and see whether or not I can use the service to write future shareholder letters. Perhaps ChatGPT has its own view of our quarter and enhanced insight.

Just to be clear, the text below was written by ChatGPT when I asked it to, “Write a Q2 2023 shareholder letter for 180 Degree Capital Corp.”:

(AUTHORED BY CHATGPT)

180 Degree Capital 123 Main Street Anytown, USA July 24, 2023

Dear Shareholders,

I hope this letter finds you well and in good spirits. It is my pleasure to share with you the highlights of our performance and progress during the second quarter of 2023.

Q2 2023 Overview:

The second quarter proved to be an eventful and successful period for 180 Degree Capital. Despite the challenges posed by a dynamic economic landscape, we continued to make strategic investments and witnessed promising developments in our portfolio companies.

Financial Performance:

I am delighted to report that our financial performance remained strong throughout the quarter. We experienced steady revenue growth across several portfolio companies, indicating a positive trajectory for the future. Our team's diligent efforts in managing costs and optimizing operational efficiency have contributed significantly to our overall financial health.

Portfolio Update:

Our investment team has been focused on identifying and nurturing promising early-stage ventures. During Q2 2023, we added several exciting companies to our portfolio, each with the potential to drive substantial returns in the long run. We are confident that these new investments align perfectly with our strategy of identifying disruptive businesses with significant growth prospects.

Furthermore, we have maintained active engagement with our existing portfolio companies, providing guidance and support to help them navigate through various challenges and capitalize on emerging opportunities. We believe in nurturing strong partnerships with the management teams of our portfolio companies, and we are confident that our approach will continue to yield positive results.

Commitment to ESG:

As a responsible and forward-thinking organization, we are committed to promoting Environmental, Social, and Governance (ESG) principles across all our investment activities. We firmly believe that integrating sustainability considerations into our decision-making process enhances long-term value for our shareholders while positively impacting society and the environment.

Outlook:

Looking ahead, we remain cautiously optimistic about the global economic landscape. We recognize that uncertainties and potential risks persist, but we are confident in our ability to adapt and navigate through changing market conditions successfully. Our commitment to staying at the forefront of innovation and identifying emerging trends will continue to drive our investment decisions.

Conclusion:

On behalf of the entire team at 180 Degree Capital, I would like to extend my heartfelt gratitude for your unwavering support and trust. Your confidence in our vision and approach inspires us to push boundaries and strive for excellence in everything we do.

As we move forward, we will continue to uphold our core values, pursue opportunities that align with our long-term goals, and remain committed to delivering value to our shareholders.

Thank you for being an essential part of our journey.

Sincerely,

[Fill in Name], Chief Executive Officer, 180 Degree Capital Corp.

(END)

Nah… Way too sugar coated and too many inaccurate comments. To start, we did not have a great quarter and ESG is not part of our investment activities. By now it should be obvious that I would never write such a letter as I have the propensity to simply tell it like it is.

Let’s try again ChatGPT… this time I asked it to, “Write a quarterly shareholder letter for 180 Degree Capital Corp. with negative performance.”:

(AUTHORED BY CHATGPT)

Dear Shareholders,

Subject: Update on Recent Quarter Performance

I hope this letter finds you well. I am writing to provide an honest and transparent assessment of our recent performance during what has undoubtedly been a challenging quarter for 180 Degree Capital Corp. Despite our best efforts and strategic planning, I regret to inform you that the results for this quarter have been disappointing.

Over the past three months, we have faced an array of unexpected hurdles that have significantly impacted our financial performance. The global economic landscape has been volatile, with various sectors experiencing uncertainty and turbulence. As a result, our portfolio companies have been subject to heightened market risks and unanticipated market fluctuations that have negatively affected our overall financial performance.

We must acknowledge that some of our investment decisions did not yield the expected returns, and our risk management strategies proved insufficient to mitigate the full impact of external market forces. While we strive for excellence and diligently analyze potential investments, the reality of investing entails inherent risks that are not always within our control.

The losses incurred during this quarter have been a sobering reminder of the importance of continuous evaluation and improvement of our investment strategies. We deeply regret any adverse impact this may have had on your investments and assure you that we are taking concrete steps to address the situation.

As a team, we have already begun an in-depth review of our investment processes to identify areas of improvement. We are actively engaging with our portfolio companies to support them during these challenging times and exploring potential opportunities for strategic realignments to bolster our future performance.

Furthermore, we are intensifying our efforts to diversify our investments to reduce overall risk exposure. Our priority remains on identifying companies with strong fundamentals, innovative business models, and robust management

teams. While this may involve adopting a more cautious approach in the short term, we are confident that it will serve the best interests of our shareholders in the long run.

As we navigate through these trying times, we firmly believe in the inherent resilience of 180 Degree Capital Corp. and remain committed to delivering long-term value to our shareholders. We understand the importance of trust and confidence, and we assure you that we are working tirelessly to regain your trust through sound decision-making and rigorous risk management practices.

In the spirit of transparency, we will be hosting a virtual shareholder meeting next month to address any concerns you may have and provide a comprehensive update on our ongoing efforts to enhance performance and drive growth.

In conclusion, I want to extend my gratitude to each and every shareholder for your continued support and belief in 180 Degree Capital Corp. We recognize the responsibility we bear, and we are steadfast in our commitment to steer the company back on a path of success and prosperity.

If you have any questions or require further information, please do not hesitate to reach out to our Investor Relations team.

Thank you for your understanding and patience during this challenging period.

Sincerely,

[Fill in Name], Chief Executive Officer, 180 Degree Capital Corp

(END)

Wow, scary… scary good and well done, ChatGPT. Much better. Not a bad shareholder letter from an imposter. It is nothing I would write, but it sounds good and would have saved me a ton of time.

Alas, while I was trying out ChatGPT, I actually thought of some inspiration for me to write about in this shareholder letter. So, let’s go that route instead of finding the perfect ChatGPT-generated letter for you to ponder.

I saw a series of posts on Twitter (or X, or whatever Elon wants to call it) on the Navy Seals from a guy named Teddy Mitrosilis that I found thought provoking and pertinent as it related to how I think about investing in general and 180 in particular. It says:

“Navy SEALs are the most elite warriors on Earth. How do they become that way? By developing an unbreakable mindset. A large part of mindset is understanding what it is, why it matters and how to apply it. In simple terms, mindset is how you view and process the world around you. It influences how we think, feel and act in situations. Our mindset is impacting us (for better or worse) every moment of every day, whether we realize it or not. The SEALs teach 3 pillars of mindset: 1. Patient, 2. Process and 3. Deliberate.

1. Patient: We must be patient in 3 ways; with ourselves, with our teammates, with the process. We are going to make mistakes. It is part of the process of growth. When we do, patience will help us work through challenges, learn, and carry on. Our teammates are human. They will also make mistakes. Getting frustrated with a teammate does not help them or you. If you want a great teammate, start by being patient.

2. Process: Everything is a process. We cannot achieve a goal on the first step, and we cannot master a skill on day 1 of practicing it. Being patient with the process helps us be consistent. Relentless consistency over time wins. SEALs training is notoriously difficult. But SEALs often say there is no single element that is extraordinarily difficult and that everyone can complete each one. It is the totality that breaks people. When do you think most people quit in SEAL training? If you guessed Hell Week you would be wrong. Most people quit on the easiest evolutions and that is the beach run (no time requirement) where the catch is you do not know when it will end. You must run until the instructors tell you to stop. So why do so many quit when all they need to do is jog lightly? Because instead of thinking about the next step they wonder when it will end. They tell themselves they can't do this for hours or longer and become overwhelmed and mentally broken. The idea is to focus on what you are doing now, not later today, not tomorrow and not next week. Practice training your mind to be in THIS moment. And remember you will fail, and it is ok to fail. Just bring yourself back. Practice this consistently and you will quickly develop the muscle.

3. Deliberate: Being deliberate is the third pillar of mindset. Being deliberate means exercising self-control with both our actions and our speech. With regards to action, for SEALs this is obvious. Every physical action can mean life or death in combat. For Navy SEALs, this is obvious. Every physical action can mean life or death in combat. Although

thankfully, for most of us this is not the case, our physical actions still matter and they keep us safe, healthy, and out of harm's way. With speech, the spoken word is powerful. If you talk to a Seal, you will notice most of them waste very few words and are extremely intentional in what they say. When things get hard, the power of our speech is amplified. Our tongue is our rudder. Pay attention to your words. What purpose do they serve? Do they supply energy or drain it? Be intentional.

Finally, when something goes wrong, the Navy SEALs look at each other and say, “FULL BENEFIT.” It's an instant mindset shift. For our normal lives, you could be hiking, and it starts pouring rain. Or you are driving, and your car breaks down. Or you are working on a project, and you lose a draft.”

For 180, it is buying a stock, the thesis changes for the worse and the stock declines. It is owning a stock that announces positive news, and its fundamentals improve, but the stock still goes down. Or, like we just experienced in Q2 2023, you have a rough quarter and lose 5.8% when your benchmark index is up 5.3%. FULL BENEFIT.

“Adversity is an opportunity to grow, to learn, to evolve, to get stronger and to become better. These moments forge us if we let them. The next time you are facing something hard, welcome it, work through the process, learn the lessons and reap the FULL BENEFIT.”

Now, I'm no Navy SEAL; not even close. They are an elite group of humans who possess extraordinary intelligence, discipline, focus, toughness, and consistency. I am, however, smart enough to know that if I apply their teachings to 180 and to investing, I’ll likely become a better investor, and the shareholders of 180 will benefit over the long term.

While we believe we own a collection of companies that we feel are poised to explode to the upside, and we come in every day hoping today is the day our performance will take off, we have, of late, left the office most days frustrated and wondering when the malaise will end. This cycle has led to thinking through a lot of SEAL teachings over the last quarter, and I keep beating them into my head on a daily basis. If there is one thing I have learned over the 30+ years of managing other people's money, it is that you do not change your stripes because your investment process is not the flavor of the day or because you had a run of challenging performance. Think like a Navy Seal. Being patient matters. Staying true to your process matters. Having discipline matters. FULL BENEFIT.

After five years of exceptional performance, the last 18 months have been extremely disappointing and frustrating. I have little desire to once again talk about the macro environment, point out how the Russell Microcap Index has underperformed every larger index in the United States, and how historically undervalued our companies are relative to themselves and to the market itself. What is most frustrating is that if you go back and read our last several shareholder letters, by and large, we have been fairly accurate with our view on how the economy will perform (we said it will be resilient). As we noted in our recent press release, “We run a highly concentrated portfolio and our returns will always be dependent on the companies we own and not only what happens with market indices” or the economy. That positioning is intentional.

It is almost comical at this point, how, no matter what news (even the good news variety) is announced by our companies, the read from the market is that such news is disregarded and has no impact on the share price or is perceived as or twisted to be negative and the stock goes down. I will provide some examples of that as this letter continues. But if there is news on Nvidia or another large-cap growth stock name…… Whatever, I get it. Because our companies are not covered as broadly as the larger cap names (that is obvious), their performance is much more unpredictable and specific company news, even positive, can go unnoticed or understood.

Unfortunately, we haven't had much great news to share with you in the last year and half, but that does not mean we will not in the second half of the year. In fact, we believe that certain catalysts could materialize over the ensuing months. These catalysts primarily center around the removal of capital structure overhangs through the refinancing of debt, completion of strategic transactions, and/or certain companies demonstrating better governance and alignment with all stakeholders. We currently believe that these catalysts, should they occur, have the potential to unlock significant value in many of our holdings.

I hope you all know me and Daniel by now. We and the rest of the management team are here for the shareholders. I happen to be the second largest shareholder of TURN, and Daniel is number six. We will always write our own shareholder letters, and we will be honest and transparent. If they are too wordy, so be it. Everyone will get the complete story from us, and they can make their own decisions about whether they want to invest in TURN. There will be no opaqueness, nor will we ever be cagey. Judging from our recent soft performance (versus excellence from our first five years) one would have thought an imposter like ChatGPT took over the management of 180 from us. They did not. Soft performance occurs. I know that because I have been working in the public markets since 1988 and managing money since 1993. We believe we have a group of highly valuable, and yet low valued businesses that are struggling to generate performance on a day-in-day-out basis. I am convinced better days are ahead for our companies and that the activism we have done (some external and some internal) will reap rewards over time. I talked above about how in this market, many of our stocks have not moved in lockstep with their improving fundamentals.

Take SNCR for example. We helped the company fix its balance sheet two years ago at a much higher price by replacing a very expensive perpetual preferred stock that limited the company’s flexibility to streamline its business with materially lower cost for financing and equity. Since then:

1.Management has run a much better business, achieving EBITDA estimates consistently higher than consensus analyst projections. Result: SNCR’s stock goes down

2.In March 2023, B. Riley presented a non-binding offer to purchase SNCR for $1.15 per share. This offer kickstarted a full strategic alternatives process. Result: SNCR’s stock cannot trade consistently above $1.00.

3.SNCR sells one of its non-core and least contributing assets that nobody even asks about when discussing the performance of the company for up to $14 million, with $7.5 million received at closing. Result: SNCR’s stock goes down.

4.In July 2023, SNCR successfully negotiated an extension of by far its largest contract to run Verizon’s personal cloud through 2030, an extension of five years. Result: SNCR’s stock increases by 2%.

Please don’t talk to me about SNCR’s aggregate revenue growth rate; the underlying business with the most value is growing and has the highest margins (70%+) of all of its businesses. Of course, every company has pluses and minuses. In the case of SNCR, however, the majority of the news has been good, not bad. The action of SNCR’s common stock is a complete head scratcher to us. I often ask myself what would have to happen to actually get SNCR to trade up? Coming up with a cure for cancer? An engine that would enable a plane to go from New York to London in two hours? It’s remarkable and frustrating all at the same time.

AREN is another one:

1.In a challenging ad environment, AREN continues to execute better than its peers with growing revenue and $100 million improvement in EBITDA. Result: AREN’s stock goes down.

2.In July 2023, the Wall Street Journal noted that Group Black is in talks to buy a stake in the company. Result: AREN’s stock increases briefly, but then resumes its decline.

3.AREN’s largest stockholder (and coincidentally largest debtholder) purchases over $1 million of AREN’s common stock in the open market. Result: AREN’s stock goes down.

Why has AREN’s stock been so weak? The only reason we can possibly come up with is that AREN has a material amount of debt on its balance sheet that technically comes due at the end of 2023. That debt is held by AREN’s largest shareholder, B. Riley, who has been purchasing common stock in the open market during this period of price weakness. Does anyone think that B. Riley would be purchasing common stock if it did not plan to renegotiate the debt and be the strong continued supporter of AREN and its common stockholders as they have always been? Are investors naïve?

The stock has cost us a nearly $1.00 drop in our NAV over the last year, and currently trades at a price that makes little sense to us. Will this decline change direction? We believe it will. When will it change? We don’t know, but we do think it will happen sooner rather than later. Value almost always wins out at the end of the day if investors have the ability to weather these weak periods.

SCOR is a similar story in that the market continues to discount the same news over and over and over again. Generally speaking, SCOR’s common stock has gone from over $5.00 to a 52-week low of $0.63 because its Board of Directors has thus far failed to act on suggestions that we and other investors have independently provided to them that we believe can reverse the trend of the shareholder destruction that has occurred under their watch. Our activism can be seen in many ways; sometimes in public letters to SCOR and other times it occurs behind the scenes. Our intention is always to be constructive and collaborative with the companies we own.

In the case of SCOR, we started with a sense of collaboration regarding our ideas for the company, but came to realize that its Board was being dismissive and unresponsive. We got back the usual “thank you for your letter, we will share it with the Board,” and then no action or only partial immaterial action would be taken. We realized quickly that the Board was supremely arrogant and seemingly lost with regards to how to create value for all stakeholders of SCOR and have instead been solely focused on creating value for preferred stockholders and themselves. The worst of the worst is the lead Independent Director, Brent Rosenthal, who has completely failed and has overseen a stock price that has declined 98% since his involvement, while at the same time receiving millions of dollars in compensation for his service as a failed Board member. The Board finally reduced its compensation by an average of 26% in 2023, but it remains above market, and the preferred stockholders are clipping coupons on their preferred stock and the board fees paid to some of SCOR’s Board who are also employees of those firms. The Board has taken small steps when more substantial action is immediately required. We have told the Board how this would play out for the common stock if they continue along their do-nothing path. We take no solace in having been right in our analysis. We just never thought they wouldn’t do anything to attack the capital structure and show better alignment amongst all stakeholders.

So, should SCOR’s Board continue to ignore their fiduciary responsibilities to common stockholders, we will resort to a series of fact-based public letters regarding the individuals on the Board who have hijacked what we believe to be SCOR’s valuable collection of data assets from the common stockholders and the employees of the company. If they don’t want to see their names attached to the level of performance they have generated over the duration of their oversight, then they should fix it with a series of actions that improve the capital structure, align themselves with common stockholders, and reverse the trend of the stock performance that has collapsed since their involvement. If they don’t want to take those steps, then they should be replaced with individuals who will take the required action. It is as simple as that. I would love nothing more than to thank them for their service and congratulate them in a public letter for taking actions that lead to the creation of shareholder value. The difference between SCOR’s Board and how we manage 180 Degree Capital is that when we have challenging quarters we tell you, we don’t excuse it, and we look for ways to act to fix it. I don’t care that we are small and the players on the Board are represented by John Malone’s Liberty Broadband, Robert Davenport at Cerberus, or Charter Communications. SCOR’s Board has a fiduciary duty to represent all stakeholders, and if they don’t want to see our public letters calling them out, then, once again, own the failure of your tenure and act now.

While it's patently obvious to anyone that the decline in the stock revolves around the inaction of SCOR’s Board, does that mean this is the right price for the business? In our view, there is no chance it is the right price. SCOR had the same structure two years ago when the stock traded around $5.00 per share. What has changed? In spite of weakness in the advertising market and increasing interest rates, SCOR’s fundamentals have materially improved. Two years ago, when the stock was $5.00, SCOR’s EBITDA was $32 million. The consensus analyst estimate according to Bloomberg for this year is $43 million and next year is $58 million. Somehow this story has evolved into an incessant, redundant, snake pit of shareholder obsession regarding the capital structure and the intentions of the preferred holders. We obviously understand the terms of the preferred stock, but we find it hard to fathom how this same “issue” is the reason for the stock to continue to decline every day. We firmly believe that $0.64 isn't the right price for the business. It would help if the Board would actually get a brain, a sense of urgency, some Wall Street smarts, some leadership and act like fiduciaries for all stakeholders. It really isn’t that complicated.

As far as the material increases and decreases in NAV this quarter, let's take a look at the individual contributors.

Largest decreases in the public portfolio in Q2 2023:1

a.Intevac, Inc. (IVAC): IVAC noted in its Q1 2023 earnings call that its program with Corning was delayed at least a quarter due to Corning's customer pushing out adoption of the new glass IVAC's tool was expected to enable. IVAC had used cash to build inventory for delivery of its tools with the expectation that the ramp would be faster than is now expected. Following that announcement, IVAC noted that Seagate cancelled over $50 million of tool orders that were expected to ship beginning in 2024. On June 13, 2023, IVAC announced its Board had retained Houlihan Lokey to explore strategic alternatives for the business. 180 sold 11% of its position at an average sale price of $7.06 per share. For the quarter, IVAC decreased NAV $0.25, or $2.5 million.

b.Comscore, Inc. (SCOR): SCOR missed estimates for Q1 2023 in what is a seasonally slow quarter, but reiterated guidance for generating free cash flow from operations and exiting 2023 with an EBITDA margin of approximately 15%. That said, SCOR's Board and its preferred stockholders did not take any steps to resolve concerns and ambiguity around the potential special dividend and misalignment between incentives for common and preferred stockholders. 180 continued its activist campaign with both public and private letters highlighting the lack of corporate governance and alignment of interests for all stakeholders to increase the price of SCOR's common stock. SCOR's preferred holders elected to defer their annual dividend of ~$15 million for future payment estimated to occur by the end of 2023, to provide additional cash for SCOR to invest in its business. For the quarter, SCOR decreased NAV by $0.21, or $2.2 million.

c.Parabellum Acquisition Partners, LLC.: Even though Parabellum Acquisition Corp, (“PRBM”) secured interest for ~$14-15 million investment from sponsors under terms that were publicly announced in mid-March 2023, on April 29, 2023, EnOcean gave notice to PRBM that it was terminating the business combination agreement between the two companies. On May 1, 2023, PRBM noted that its sponsors declined to invest additional capital to extend the life of the SPAC and it entered the process of liquidating the trust and winding down operations. 180 does not currently expect to receive any proceeds from the liquidation process of PRBM or its sponsor. For the quarter, Parabellum Acquisition Partners decreased NAV by $0.20, or $2 million.

Largest increases in the public portfolio in Q2 2023:1

a.Commercial Vehicle Group, Inc. (CVGI): CVGI reported better than expected results for Q1 2023 that included better pricing from its remaining contracts that were renegotiated in the quarter and the company provided overall strong guidance for the remainder of 2023. 180 sold 28% of its position at an average sale price per share of $10.31. For the quarter, CVGI increased NAV by $0.18, or $1.9 million.

_____________________

1. On an daily average shares outstanding basis during the period of 10,268,529.

b.D-Wave Quantum, Inc. (QBTS): QBTS reported weak results for the first quarter and a new debt facility from its largest shareholder for up to $50 million, with $15 million drawn initially and the next tranches available if the company achieves certain milestones. After selling off materially following earnings, QBTS appears to be the beneficiary of interest in AI-related stocks, and its stock price increased dramatically from the lows following earnings. With the stock above $1/share, QBTS now has access to its equity facility from Lincoln Park Capital. For the quarter, QBTS increased NAV by $0.11, or $1.2 million.

c.Potbelly Corporation (PBPB): PBPB pre-announced strong results for Q1 2023, across all financial and shop-level metrics that exceeded expectations and guidance. Its stock subsequently rose to a high over $11 per share during the quarter. 180 sold an additional 7% of its position at an average price of $8.96. After holding its full results in May 2023, PBPB's stock collapsed from $11 per share to $8 per share. While PBPB's results were positive overall, its lone analyst, Baird, materially reduced its earnings expectations for future years. Following this collapse, 180 purchased an additional 18,813 shares at an average price per share of $8.08. For the quarter, PBPB increased NAV by $0.07, or $0.7 million.

NET ASSET VALUE PER SHARE

Our NAV decreased this quarter from $6.52 to $6.22, a decrease of 4.6%. Our Fund has three principal components to the variance in our NAV: our public and public-related portfolio, our legacy private portfolio, and our expenses. For the quarter, our public and public related portfolio companies decreased our NAV by $0.34, our remaining private portfolio increased our NAV by $0.06, and our operating expenses decreased NAV by $0.08. In addition, the share repurchase program we initiated increased our NAV by $0.06.

| | | | | | | | | | | | | | | | | | | | |

| Quarter | YTD | 1 Year | 3 Year | 5 Year | Inception to Date |

| Q2 2023 | Q4 2022- Q2 2023 | Q2 2022- Q2 2023 | Q2 2020- Q2 2023 | Q2 2018- Q2 2023 | Q4 2016- Q2 2023 |

| | | | | | |

| | | | | | |

| | | | | | |

| Change in NAV | (4.6%) | (1.6%) | (25.5%) | (23.2%) | (28.8%) | (11.4%) |

| | | | | | |

| Change in Stock Price | (11.5%) | (15.7%) | (27.4%) | (14.8%) | (35.8%) | 7.5% |

| | | | | | |

| Russell Microcap Index | 5.3% | 2.3% | 6.6% | 29.7% | 10.6% | 38.7% |

| Russell Microcap Value Index | 4.8% | (0.7%) | 3.2% | 57.1% | 18.9% | 47.1% |

| Russell 2000 | 5.2% | 8.1% | 12.3% | 36.0% | 22.7% | 51.4% |

| | | | | | |

| | | | | | |

| | | | | | |

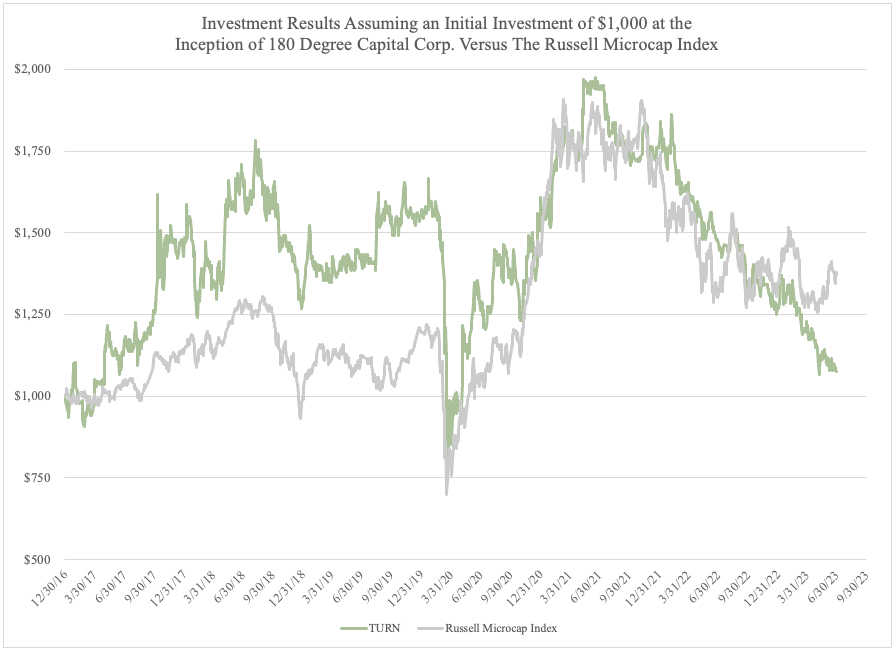

On a relative basis, TURN's stock price total return of +7.5% trailed the Russell Microcap Index total return of +38.7% since our inception as is shown in the chart below:

PUBLIC AND RELATED PORTFOLIO

In the chart below, you see our Q2 2023, YTD, one-year, three-year, five-year, and inception-to-date performance.

| | | | | | | | | | | | | | | | | | | | |

| Quarter | YTD | 1 Year | 3 Year | 5 Year | Inception to Date |

| Q2 2023 | Q4 2022- Q2 2023 | Q2 2022- Q2 2023 | Q2 2020- Q2 2023 | Q2 2018- Q2 2023 | Q4 2016- Q2 2023 |

TURN Public Portfolio

Gross Total Return (Excluding SMA Carried Interest) | (5.8%) | (0.5%) | (10.0%) | 10.6% | 31.9% | 203.7% |

TURN Public Portfolio

Gross Total Return (Including SMA Carried Interest) | (5.8%) | (0.5%) | (10.0%) | 18.0% | 40.8% | 223.6% |

| | | | | | |

| | | | | | |

| | | | | | |

| | | | | | |

| | | | | | |

| Russell Microcap Index | 5.3% | 2.3% | 6.6% | 29.7% | 10.6% | 38.7% |

| Russell Microcap Value Index | 4.8% | (0.7%) | 3.2% | 57.1% | 18.9% | 47.1% |

| Russell 2000 | 5.2% | 8.1% | 12.3% | 36.0% | 22.7% | 51.4% |

| | | | | | |

| | | | | | |

| | | | | | |

We have achieved a +223.6% gross total return since the inception of 180 versus +38.7 % total return for the Russell Microcap Index, which we believe is a good period of time to evaluate whether or not we are good at what we say we are trying to do. The market for microcaps is filled with inefficiencies and asymmetric risk/reward characteristics. If you get your stock picking right, you can achieve outsized returns. Based on our research and analysis, we believe many of the individual companies we own have upside of 100% over a three-year period. We have permanent capital and the opportunity to take advantage of the current dislocation is easier for us because we don’t have to sell to service redemptions. Our permanent capital allows us to make rational decisions on our investments, and we believe this is a distinct advantage in regard to our ability to generate returns greater than the indices over an investment cycle. We are never forced to sell unless we believe we should for analytical and investment process reasons. We have seen the benefits of having permanent capital and our overall approach to investing since our inception, but we also aren't immune from periods of soft performance; we're living through one of those periods right now. Our -5.8% gross total return compared unfavorably with the +5.3% return for the Russell Microcap Index. Year-to-date, our -0.5% return is slightly behind the Russell Microcap Index return of +2.3% and slightly above the -0.7% return for the

Russell Microcap Value Index. We have intentionally created a concentrated portfolio that has very low correlation to the broad indices. We are aware of the potential for episodic returns for our holdings. We believe TURN will see gains from most of our investments, however we just can't say when.

LEGACY PRIVATE PORTFOLIO

180’s remaining private portfolio has only one material position, AgBiome. The total value of our remaining legacy private portfolio is approximately $8.6 million, of which approximately $6.2 million is AgBiome, and approximately $1.3 million are cash proceeds that we expect to receive in April 2024 from the sale of TARA Biosystems, Inc., to Valo Health, LLC. This past quarter, we had a markup in AgBiome based on market adjustment factors derived from comparable public companies. In total, the private portfolio increased our NAV by $0.06 this quarter. There really is not much more to add regarding the legacy portfolio as it now represents just 13.7% of our net assets. We took a business that was headed to zero and created a new business with a real future and a stable balance sheet.

EXPENSES

For Q2 2023 our regular operating expenses equaled approximately $879,000 versus approximately $741,000 in Q2 2022. We will maintain a lean cost structure (outside of fixed expenses for being a public company) focusing our expenses on activities solely designed to enhance our investment performance or to increase our revenues from managing outside capital. The increase in operating expenses was due primarily to the addition of Matt Epstein to our investment team late last summer. Matt brings a fresh perspective and complementary set of skills to the team, and we are pleased to have him aboard.

SHARE BUYBACK

We have spoken for a long time about our desire to be in a position to return capital to shareholders. While we recognize the importance of permanent capital, we decided to start making purchases from our announced share repurchase program and repurchased of a block of stock that was for sale. Buying a stock at $4.41 (excluding brokerage commissions) when NAV is more than 30% higher was accretive to our NAV, and such a repurchase should send a signal that we are serious about creating value for our shareholders. We find it remarkable that given all we have done to remake our balance sheet; we still trade at virtually the same discount to NAV that we had when the majority of our assets were in opaque private holdings. The cash outlay for this repurchase was less than 2.5% of our liquid assets, and we hope this is a message to shareholders that our share price is our number one priority. Our Board of Directors recently reauthorized the size of the share repurchase program to provide us with continued flexibility to take advantage of further extreme dislocations between our NAV and stock price.

CONCLUSION

While we are frustrated with our performance in Q2 2023, we used the quarter to position TURN to benefit should certain catalysts of our holdings occur down the road. We believe several catalysts may occur in the second half of 2023, and we will continue to use our constructive activism to drive these events to completion where possible. We will attempt to make ourselves smarter by adhering to the valuable lessons for how the Navy SEALs operate. Rather than waste time and energy whining about Q2 2023, we continue to believe there will be a day when we reap the FULL BENEFIT from taking actions designed to create value for TURN’s stockholders over time. As a reminder, I don’t own 667,440 shares of TURN stock purchased in the open market with after-tax dollars for kicks.

As always, thank you for your support.

Best Regards,

Kevin Rendino

Chairman and Chief Executive Officer

Forward-Looking Statements and Disclaimers

This shareholder letter may contain statements of a forward-looking nature relating to future events. These forward-looking statements are subject to the inherent uncertainties in predicting future results and conditions. These statements reflect the Company's current beliefs, and a number of important factors could cause actual results to differ materially from those expressed in this press release. Please see the Company's securities filings filed with the Securities and Exchange Commission for a more detailed discussion of the risks and uncertainties associated with the Company's business and other significant factors that could affect the Company's actual results. Except as otherwise required by Federal securities laws, the Company undertakes no obligation to update or revise these forward-looking statements to reflect new events or uncertainties. The

reference and link to any websites have been provided as a convenience, and the information contained on such website is not incorporated by reference into this shareholder letter. 180 Degree Capital Corp. is not responsible for the contents of third-party websites. The information discussed above is solely the opinion of 180 Degree Capital Corp. Any discussion of past performance is not an indication of future results. Investing in financial markets involves a substantial degree of risk. Investors must be able to withstand a total loss of their investment. The information herein is believed to be reliable and has been obtained from sources believed to be reliable, but no representation or warranty is made, expressed or implied, with respect to the fairness, correctness, accuracy, reasonableness or completeness of the information and opinions.

| | |

180 DEGREE CAPITAL CORP.

CONSOLIDATED STATEMENT OF ASSETS AND LIABILITIES (UNAUDITED) |

| | | | | |

| | June 30, 2023 |

| ASSETS | |

| Investments in securities and other financial instruments, at value: | |

| Unaffiliated publicly traded equity and equity-related securities (cost: $32,529,020) | $ | 26,013,273 | |

| Unaffiliated legacy privately held equity and equity-related securities (cost: $8,875,116) | 6,573,355 | |

| Non-controlled affiliated publicly traded equity and equity-related securities (cost: $39,846,136) | 26,983,897 | |

| Non-controlled affiliated legacy privately held equity and equity-related securities (cost: $6,496,930) | 203,436 | |

| Controlled affiliated equity and equity-related securities (cost: $2,923,003) | 0 | |

| Unaffiliated derivative securities (cost: $113,639) | 0 | |

| Non-controlled affiliated derivative securities (cost: $224,849) | 419,795 | |

| Unaffiliated rights to payments (cost: $2,252,034) | 1,822,420 | |

| Unaffiliated money market fund securities (cost: $120,517) | 120,517 | |

| Cash | 376,397 | |

| Receivable from securities sold | 261,217 | |

| Receivable from managed funds | 152,151 | |

| Prepaid expenses | 131,922 | |

| Lease asset | 54,296 | |

| Other assets | 23,517 | |

| Other receivables | 3,198 | |

| Total assets | $ | 63,139,391 | |

| LIABILITIES & NET ASSETS | |

| |

| Post-retirement plan liabilities | $ | 624,296 | |

| Accounts payable and accrued liabilities | 250,296 | |

| Lease obligation | 54,296 | |

| Total liabilities | $ | 928,888 | |

| Commitments and contingencies (Note 10) | |

| Net assets | $ | 62,210,503 | |

| Net assets are comprised of: | |

| Preferred stock, $0.10 par value, 2,000,000 shares authorized; none issued | $ | 0 | |

| Common stock, $0.03 par value, 15,000,000 shares authorized; 11,541,079 issued | 334,594 | |

| Additional paid in capital | 115,687,138 | |

| Total accumulated distributable loss | (47,550,306) | |

| Treasury stock, at cost 1,540,938 shares | (6,260,923) | |

| Net assets | $ | 62,210,503 | |

| Shares outstanding | 10,000,141 | |

| Net asset value per outstanding share | $ | 6.22 | |

The accompanying notes are an integral part of these unaudited consolidated financial statements.

12

| | |

180 DEGREE CAPITAL CORP.

CONSOLIDATED STATEMENT OF OPERATIONS (UNAUDITED) |

| | | | | |

| Six Months Ended

June 30, 2023 |

| Income: | |

| Dividend | $ | 27,653 | |

| Interest-Unaffiliated money market fund securities | 21,594 | |

| Total income | 49,247 | |

| Operating fees and expenses: | |

| Salaries, bonus and benefits | 991,957 | |

| Professional | 261,703 | |

| Administration and operations | 243,374 | |

| Directors | 137,267 | |

| Insurance | 115,716 | |

| Rent | 17,598 | |

| Custody | 15,999 | |

| Other | 4,825 | |

| Total operating expenses | 1,788,439 | |

| Net investment loss before income tax expense | (1,739,192) | |

| Income tax expense | 808 | |

| Net investment loss | (1,740,000) | |

| Net realized gain (loss) from investments: | |

| Unaffiliated publicly traded equity and equity-related securities | 5,059,957 | |

| Unaffiliated legacy privately held equity and equity-related securities | (233,845) | |

| Non-controlled affiliated publicly traded equity and equity-related securities | 980,569 | |

| Net realized gain from investments | 5,806,681 | |

| Sale of equity-180 Degree Capital BD, LLC (Note 2) | 100,000 | |

| Net realized gain | 5,906,681 | |

| Change in unrealized (depreciation) appreciation on investments: | |

| Unaffiliated publicly traded equity and equity-related securities | (2,976,877) | |

| Unaffiliated legacy privately held equity and equity-related securities | 295,212 | |

| Non-controlled affiliated publicly traded equity and equity-related securities | (550,352) | |

| Non-controlled affiliated legacy privately held equity and equity-related securities | 44,550 | |

| Controlled affiliated equity and equity-related securities | (2,706,572) | |

| Unaffiliated rights to payments | 48,110 | |

| Net change in unrealized depreciation on investments | (5,845,929) | |

| Net realized gain and change in unrealized depreciation on investments | 60,752 | |

| Net decrease in net assets resulting from operations | $ | (1,679,248) | |

The accompanying notes are an integral part of these unaudited consolidated financial statements.

13

| | |

180 DEGREE CAPITAL CORP.

CONSOLIDATED STATEMENT OF CASH FLOWS (UNAUDITED) |

| | | | | |

| Six Months Ended

June 30, 2023 |

| Cash flows provided by operating activities: | |

| Net decrease in net assets resulting from operations | $ | (1,679,248) | |

| Adjustments to reconcile net decrease in net assets resulting from operations to net cash provided by operating activities: |

| Net realized gain from investments | (5,906,681) | |

| Net change in unrealized depreciation on investments | 5,845,929 | |

| Depreciation of fixed assets | 4,936 | |

| Purchase of unaffiliated publicly traded equity and equity-related securities | (14,145,056) | |

| Purchase of non-controlled affiliated publicly traded equity and equity-related securities | (1,906,745) | |

| Purchase of unaffiliated money market fund securities | (120,517) | |

| Proceeds from sale of unaffiliated publicly traded equity and equity-related securities | 16,384,315 | |

| Proceeds from sale of non-controlled affiliated publicly traded and equity-related securities | 2,233,267 | |

| Distribution from unaffiliated rights to payments | 1,068,504 | |

| Proceeds from sale equity of 180 Degree Capital BD, LLC | 100,000 | |

| Changes in assets and liabilities: | |

| Decrease in prepaid expenses | 118,517 | |

| Increase in receivable from securities sold | (152,705) | |

| Increase in other assets | (3,304) | |

| Increase in other receivables | (920) | |

| Decrease in post-retirement plan liabilities | (21,341) | |

| Decrease in accounts payable and accrued liabilities | (227,921) | |

| Decrease in payable for securities purchased | (210,971) | |

| Net cash provided by operating activities | 1,380,059 | |

| Cash flows from investing activities | |

| Purchase of fixed assets | (3,723) | |

| Net cash used in investing activities | (3,723) | |

| Cash flows from financing activities | |

| Purchase of treasury stock | (1,655,398) | |

| Net cash used in financing activities | (1,655,398) | |

| Net decrease in cash | (279,062) | |

| Cash at beginning of the period/year | 655,459 | |

| Cash at end of the period/year | $ | 376,397 | |

| Supplemental disclosures of cash flow information: | |

| Income taxes paid | $ | 808 | |

| |

The accompanying notes are an integral part of these unaudited consolidated financial statements.

14

| | |

180 DEGREE CAPITAL CORP.

CONSOLIDATED STATEMENTS OF CHANGES IN NET ASSETS |

| | | | | | | | | | | |

| Six Months Ended

June 30, 2023 | | Year Ended December 31, 2022 |

| UNAUDITED | | |

| Changes in net assets from operations: | | | |

| Net investment loss | $ | (1,747,000) | | | $ | (2,583,203) | |

| Net realized gain | 5,906,681 | | | 2,204,654 | |

| Net change in unrealized depreciation on investments | (5,845,929) | | | (44,652,254) | |

| Net decrease in net assets resulting from operations | (1,686,248) | | | (45,030,803) | |

| | | |

| Changes in net assets from capital stock transactions: | | | |

| Treasury stock purchase | (1,655,398) | | | 0 | |

| Net decrease in net assets resulting from capital stock transactions | (1,655,398) | | | 0 | |

| Net decrease in net assets | (3,341,646) | | | (45,030,803) | |

| Net Assets: | | | |

| Beginning of the period/year | 65,545,149 | | | 110,575,952 | |

| End of the period/year | $ | 62,203,503 | | | $ | 65,545,149 | |

| | | |

The accompanying notes are an integral part of these unaudited consolidated financial statements.

15

| | |

180 DEGREE CAPITAL CORP.

CONSOLIDATED FINANCIAL HIGHLIGHTS |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Six Months Ended June 30, 2023 | | Year Ended Dec. 31, 2022 | | Year Ended Dec. 31, 2021 | | Year Ended Dec. 31 2020# | | Year Ended Dec. 31 2019# | | Year Ended Dec. 31, 2018# | | | | |

| (UNAUDITED) | | | | | | | | | | | | | | |

| Per Share Operating Performance: | | | | | | | | | | | | | | | |

| Net asset value per share, beginning of the period/year | $ | 6.32 | | | $ | 10.66 | | | $ | 9.28 | | | $ | 9.18 | | | $ | 7.92 | | | $ | 7.80 | | | | | |

Net investment loss* | (0.17) | | | (0.25) | | | (0.33) | | | (0.05) | | | (0.48) | | | (0.21) | | | | | |

Net realized gain (loss) from investments* | 0.58 | | | 0.21 | | | 0.20 | | | (0.11) | | | 0.93 | | | (0.75) | | | | | |

Net change in unrealized (depreciation) appreciation on investments and options*1 | (0.57) | | | (4.30) | | | 1.51 | | | 0.26 | | | 0.81 | | | 1.08 | | | | | |

| Total from investment operations* | (0.16) | | | (4.34) | | | 1.38 | | | 0.10 | | | 1.26 | | | 0.12 | | | | | |

| | | | | | | | | | | | | | | |

| Net increase as a result of purchase of treasury stock | 0.06 | | | 0.00 | | | 0.00 | | | 0.00 | | | 0.00 | | | 0.00 | | | | | |

| Net (decrease) increase in net asset value | (0.10) | | | (4.34) | | | 1.38 | | | 0.10 | | | 1.26 | | | 0.12 | | | | | |

| Net asset value per share, end of the period/year | $ | 6.22 | | | $ | 6.32 | | | $ | 10.66 | | | $ | 9.28 | | | $ | 9.18 | | | $ | 7.92 | | | | | |

| | | | | | | | | | | | | | | |

| Stock price per share, end of the period/year | $ | 4.45 | | | $ | 5.28 | | | $ | 7.35 | | | $ | 6.66 | | | $ | 6.45 | | | $ | 5.25 | | | | | |

| Total return based on stock price | (15.72) | % | | (28.16) | % | | 10.36 | % | | 3.26 | % | | 22.86 | % | | (11.17) | % | | | | |

| Supplemental Data: | | | | | | | | | | | | | | | |

| Net assets, end of the period/year | $ | 62,203,503 | | | $ | 65,545,149 | | | $ | 110,575,952 | | | $ | 96,317,794 | | | $ | 95,213,639 | | | $ | 82,034,768 | | | | | |

| Ratio of expenses to average net assets | 2.76 | % | 2 | 3.20 | % | ^ | 5.87 | % | ^ | 4.61 | % | ^ | 6.42 | % | ^ | 3.63 | % | ^ | | | |

| Ratio of net investment loss to average net assets | (2.19) | % | 2 | (2.88) | % | | (3.26) | % | | (0.59) | % | | (5.42) | % | | (2.82) | % | | | | |

| Portfolio turnover | 24.71 | % | | 30.95 | % | | 44.46 | % | | 35.16 | % | | 30.17 | % | | 20.43 | % | | | | |

| Number of shares outstanding, end of the period/year | 10,000,141 | | | 10,373,820 | | | 10,373,820 | | | 10,373,820 | | | 10,373,820 | | | 10,373,820 | | | | | |

# Reflect a 1-for-3 reverse stock split that became effective on January 4, 2021.

* Based on average shares outstanding.

^ The Company has entered into an expense offsetting arrangement with one of its unaffiliated brokers relating to broker fees paid. The total broker fee charged to the Company was applied as a credit to fees charged by an affiliate of the unaffiliated broker who the Company subscribes to for data services billed during the year. The Company received an offset to expense totaling approximately $20,600, $84,800, $31,900, $15,700, and $17,500 with that broker for the years ended December 31, 2022-2018, respectively.

1 Net unrealized losses include rounding adjustments to reconcile change in net asset value per share.

2 Not annualized.

The accompanying notes are an integral part of these unaudited consolidated financial statements.

16

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| 180 DEGREE CAPITAL CORP. CONSOLIDATED SCHEDULE OF INVESTMENTS AS OF JUNE 30, 2023 (UNAUDITED) |

| | | | | | | | | |

| Method of

Valuation (1) | | Industry | | Shares/Units | | Cost | | Value |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Investments in Unaffiliated Equity and Equity-Related Securities (2) - | | | | | | | | | |

| 52.6% of net assets at value | | | | | | | | | |

| | | | | | | | | |

| Unaffiliated Publicly Traded Equity and Equity-Related Securities - | | | | | | | | | |

| 41.8% of net assets at value | | | | | | | | | |

| | | | | | | | | |

| Ascent Industries Co. (3) | | | Steel | | | | | | |

| Manufactures metals and chemicals | | | | | | | | | |

| Common Stock | (M) (L2) | | | | 300,435 | | $ | 3,198,566 | | | $ | 2,730,954 | |

| | | | | | | | | |

| Brightcove, Inc. (3) | | | Internet Services & Infrastructure | | | | | | |

| Provides video hosting and publishing services | | | | | | | | | |

| Common Stock | (L1) | | | | 265,900 | | 1,306,454 | | | 1,066,259 | |

| | | | | | | | | |

| Commercial Vehicle Group, Inc. (3) | | | Construction Machinery & Heavy Trucks | | | | | | |

| Supplier of vehicle components | | | | | | | | | |

| Common Stock | (L1) | | | | 376,136 | | 2,189,776 | | | 4,175,110 | |

| | | | | | | | | |

| D-Wave Quantum, Inc. (3)(4) | | | Technology Hardware, Storage & Peripherals | | | | | | |

| Develops high-performance quantum computing systems | | | | | | | | | |

| Common Stock | (L1) | | | | 770,000 | | 1,045,355 | | | 1,609,300 | |

| | | | | | | | | |

| Intevac, Inc. (3) | | | Technology Hardware, Storage & Peripherals | | | | | | |

| Develops solutions for the application and engineering of thin-films | | | | | | | | | |

| Common Stock | (L1) | | | | 939,337 | | 4,337,708 | | | 3,522,514 | |

| | | | | | | | | |

| Lantronix, Inc. (3) | | | Communications Equipment | | | | | | |

| Provides secure data access and management solutions | | | | | | | | | |

| Common Stock | (L1) | | | | 746,413 | | 3,795,733 | | | 3,142,399 | |

| | | | | | | | | |

| | | | | | | | | |

| | | | | | | | | |

| | | | | | | | | |

| | | | | | | | | |

The accompanying notes are an integral part of these unaudited consolidated financial statements.

17

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| 180 DEGREE CAPITAL CORP. CONSOLIDATED SCHEDULE OF INVESTMENTS AS OF JUNE 30, 2023 (UNAUDITED) |

| | | | | | | | | |

| Method of

Valuation (1) | | Industry | | Shares/Units | | Cost | | Value |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Investments in Unaffiliated Equity and Equity-Related Securities (2) - | | | | | | | | | |

| 52.6% of net assets at value (cont.) | | | | | | | | | |

| | | | | | | | | |

| Unaffiliated Publicly Traded Equity and Equity-Related Securities - | | | | | | | | | |

| 41.8% of net assets at value (cont.) | | | | | | | | | |

| | | | | | | | | |

| MamaMancini's Holdings, Inc. (3) | | | Packaged Foods & Meats | | | | | | |

| Sells specialty pre-prepared and refigerated foods | | | | | | | | | |

| Common Stock | (L1) | | | | 578,989 | | $ | 1,447,473 | | | $ | 1,748,547 | |

| | | | | | | | | |

| Quantum Corporation (3) | | | Technology Hardware, Storage & Peripherals | | | | | | |

| Provides high-density data storage and high-speed data processing solutions | | | | | | | | | |

| Common Stock | (L1) | | | | 3,221,192 | | 8,787,175 | | | 3,478,887 | |

| | | | | | | | | |

| Rayonier Advanced Materials, Inc. (3) | | | Specialty Chemicals | | | | | | |

| Produces specialty cellulose fibers | | | | | | | | | |

| Common Stock | (L1) | | | | 652,826 | | 3,665,500 | | | 2,794,095 | |

| | | | | | | | | |

| RF Industries, Ltd. (3) | | | Electronic Manufacturing Services | | | | | | |

| Provides products that enable wired and wireless communications | | | | | | | | | |

| Common Stock | (L1) | | | | 420,532 | | 2,755,280 | | | 1,745,208 | |

| | | | | | | | | |

| Total Unaffiliated Publicly Traded Equity and Equity-Related Securities (cost: $32,529,020) | | | | | | | | | $ | 26,013,273 | |

| | | | | | | | | |

The accompanying notes are an integral part of these unaudited consolidated financial statements.

18

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| 180 DEGREE CAPITAL CORP. CONSOLIDATED SCHEDULE OF INVESTMENTS AS OF JUNE 30, 2023 (UNAUDITED) |

| | | | | | | | | |

| Method of

Valuation (1) | | Industry | | Shares/Units | | Cost | | Value |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Investments in Unaffiliated Equity and Equity-Related Securities (2) - | | | | | | | | | |

| 52.6% of net assets at value (cont.) | | | | | | | | | |

| | | | | | | | | |

| Unaffiliated Money Market Fund Securities - | | | | | | | | | |

| 0.2% of net assets at value | | | | | | | | | |

| | | | | | | | | |

| JPMorgan 100% U.S. Treasury Securities Money Market Fund - Capital | | | | | | | | | |

| Common Stock (Yield 4.99%) | (L1) | | | | 120,517 | | | $ | 120,517 | | | $ | 120,517 | |

| | | | | | | | | |

| Total Unaffiliated Money Market Fund Securities (cost: $120,517) | | | | | | | | | $ | 120,517 | |

| | | | | | | | | |

| Unaffiliated Legacy Privately Held Equity and Equity-Related Securities - | | | | | | | | | |

| 10.6% of net assets at value | | | | | | | | | |

| | | | | | | | | |

| AgBiome, LLC (3)(5) | | | Fertilizers & Agricultural Chemicals | | | | | | |

| Develops agricultural products that reduce risk and improve yield | | | | | | | | | |

| Series A-1 Convertible Preferred Units (acquired 1/30/13) | (H) (L3) | | | | 2,000,000 | | $ | 2,000,000 | | | $ | 4,780,742 | |

| Series A-2 Convertible Preferred Units (acquired 4/9/13-10/15/13) | (H) (L3) | | | | 417,392 | | 521,740 | | | 999,110 | |

| Series B Convertible Preferred Units (acquired 8/7/15) | (H) (L3) | | | | 160,526 | | 500,006 | | | 398,249 | |

| | | | | | | | 3,021,746 | | | 6,178,101 | |

| | | | | | | | | |

| AutoTech Ventures Management I, LLC (5)(6) | | | Asset Management & Custody Banks | | | | | | |

| Venture capital investing in automotive-related companies | | | | | | | | | |

| LLC Interests (acquired 12/1/17) | (M) (L3) | | | | 0 | | 0 | | | 218,534 | |

| | | | | | | | | |

| Magnolia Neurosciences Corporation (3)(5)(7)(8) | | | Pharmaceuticals | | | | | | |

| Develops novel therapeutics for treatment of neurodegeneration | | | | | | | | | |

| Series A Convertible Preferred Stock (acquired 8/3/18) | (I) (L3) | | | | 862,872 | | 748,536 | | | 121,108 | |

| | | | | | | | | |

The accompanying notes are an integral part of these unaudited consolidated financial statements.

19

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| 180 DEGREE CAPITAL CORP. CONSOLIDATED SCHEDULE OF INVESTMENTS AS OF JUNE 30, 2023 (UNAUDITED) |

| | | | | | | | | |

| Method of

Valuation (1) | | Industry | | Shares/Units | | Cost | | Value |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Investments in Unaffiliated Equity and Equity-Related Securities (2) - | | | | | | | | | |

| 52.6% of net assets at value (cont.) | | | | | | | | | |

| | | | | | | | | |

| Unaffiliated Legacy Privately Held Equity and Equity-Related Securities - | | | | | | | | | |

| 10.6% of net assets at value (cont.) | | | | | | | | | |

| | | | | | | | | |

| Nanosys, Inc. (3)(5)(7)(9) | | | Specialty Chemicals | | | | | | |

| Develops inorganic nanowires and quantum dots for use in LED-backlit devices | | | | | | | | | |

| Series A-1 Convertible Preferred Stock (acquired 5/22/21) | (I) (L3) | | | | 496,572 | | $ | 496,573 | | | $ | 23,058 | |

| Series A-2 Convertible Preferred Stock (acquired 5/22/21) | (I) (L3) | | | | 2,232,001 | | 4,500,003 | | | 16,140 | |

| | | | | | | | 4,996,576 | | | 39,198 | |

| | | | | | | | | |

| Ravenna Pharmaceuticals, Inc. (3)(5)(7)(8)(10) | | | Pharmaceuticals | | | | | | |

| Holding company for intellectual property in oncology therapeutics | | | | | | | | | |

| Common Stock (acquired 5/14/20-8/26/21) | (M) (L3) | | | | 2,785,274 | | 108,258 | | | 16,414 | |

| | | | | | | | | |

| Total Unaffiliated Legacy Privately Held Equity and Equity-Related Securities (cost: $8,875,116) | | | | | | | | | $ | 6,573,355 | |

| | | | | | | | | |

| Total Investments in Unaffiliated Equity and Equity-Related Securities (cost: $41,524,653) | | | | | | | | | $ | 32,707,145 | |

| | | | | | | | | |

The accompanying notes are an integral part of these unaudited consolidated financial statements.

20

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| 180 DEGREE CAPITAL CORP. CONSOLIDATED SCHEDULE OF INVESTMENTS AS OF JUNE 30, 2023 (UNAUDITED) |

| | | | | | | | | |

| Method of

Valuation (1) | | Industry | | Shares/Units | | Cost | | Value |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Investments in Non-Controlled Affiliated Equity and Equity-Related Securities (2) - | | | | | | | | | |

| 43.7% of net assets at value | | | | | | | | | |

| | | | | | | | | |

| Non-Controlled Affiliated Publicly Traded Equity and Equity-Related Securities - | | | | | | | | | |

| 43.4% of net assets at value | | | | | | | | | |

| | | | | | | | | |

| Arena Group Holdings, Inc. (3)(11) | | | Interactive Media & Services | | | | | | |

| Provides a shared digital publishing, advertising and distribution platform | | | | | | | | | |

| Common Stock | (L1) | | | | 989,464 | | $ | 9,803,214 | | | $ | 4,531,745 | |

| | | | | | | | | |

| Comscore, Inc. (3)(11) | | | Advertising | | | | | | |

| Provides technology and services that measure audiences, brands and consumer behavior | | | | | | | | | |

| Common Stock | (L1) | | | | 5,949,217 | | 11,757,108 | | | 4,818,866 | |

| | | | | | | | | |

| Potbelly Corporation (3)(11) | | | Restaurants | | | | | | |

| Operates a chain of sandwich shops | | | | | | | | | |

| Common Stock | (L1) | | | | 1,343,332 | | 6,127,504 | | | 11,794,455 | |

| | | | | | | | | |

| Synchronoss Technologies, Inc. (3)(11) | | | Application Software | | | | | | |

| Provides white-label cloud storage, messaging and other digital analytic services | | | | | | | | | |

| Common Stock | (L1) | | | | 6,284,395 | | 12,158,310 | | | 5,838,831 | |

| | | | | | | | | |

| Total Non-Controlled Affiliated Publicly Traded Equity and Equity-Related Securities (cost: $39,846,136) | | | | | | | | | $ | 26,983,897 | |

| | | | | | | | | |

The accompanying notes are an integral part of these unaudited consolidated financial statements.

21

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| 180 DEGREE CAPITAL CORP. CONSOLIDATED SCHEDULE OF INVESTMENTS AS OF JUNE 30, 2023 (UNAUDITED) |

| | | | | | | | | |

| Method of

Valuation (1) | | Industry | | Shares/Units | | Cost | | Value |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Investments in Non-Controlled Affiliated Equity and Equity-Related Securities (2) - | | | | | | | | | |

| 43.7% of net assets at value (cont.) | | | | | | | | | |

| | | | | | | | | |

| Non-Controlled Affiliated Legacy Privately Held Equity and Equity-Related Securities - | | | | | | | | | |

| 0.3% of net assets at value | | | | | | | | | |

| | | | | | | | | |

| EchoPixel, Inc. (3)(5)(7) | | | Health Care Equipment | | | | | | |

| Develops virtual reality 3-D visualization software for life sciences and health care applications | | | | | | | | | |

| Series Seed Convertible Preferred Stock (acquired 6/21/13-6/30/14) | (I) (L3) | | | | 4,194,630 | | $ | 1,250,000 | | | $ | 104,680 | |

| Series Seed-2 Convertible Preferred Stock (acquired 1/22/16) | (I) (L3) | | | | 1,476,668 | | 500,000 | | | 37,688 | |

| Series A-2 Convertible Preferred Stock (acquired 3/23/17) | (I) (L3) | | | | 1,471,577 | | 350,000 | | | 61,068 | |

| | | | | | | | 2,100,000 | | | 203,436 | |

| | | | | | | | | |

| HALE.life Corporation (3)(5)(7) | | | Health Care Technology | | | | | | |

| Develops a platform to facilitate precision health and medicine | | | | | | | | | |

| Common Stock (acquired 3/1/16) | (I) (L3) | | | | 1,000,000 | | 10 | | | 0 | |

| Series Seed-1 Convertible Preferred Stock (acquired 3/28/17) | (I) (L3) | | | | 11,000,000 | | 1,896,920 | | | 0 | |

| Series Seed-2 Convertible Preferred Stock (acquired 12/28/18) | (I) (L3) | | | | 12,083,132 | | 2,500,000 | | | 0 | |

| | | | | | | | 4,396,930 | | | 0 | |

| | | | | | | | | |

| Total Non-Controlled Affiliated Legacy Privately Held Equity and Equity-Related Securities (cost: $6,496,930) | | | | | | | | | $ | 203,436 | |

| | | | | | | | | |

| Total Investments in Non-Controlled Affiliated Equity and Equity-Related Securities (cost: $46,343,066) | | | | | | | | | $ | 27,187,333 | |

| | | | | | | | | |

The accompanying notes are an integral part of these unaudited consolidated financial statements.

22

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| 180 DEGREE CAPITAL CORP. CONSOLIDATED SCHEDULE OF INVESTMENTS AS OF JUNE 30, 2023 (UNAUDITED) |

| | | | | | | | | |

| Method of

Valuation (1) | | Industry | | Shares/Units | | Cost | | Value |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Controlled Affiliated Equity and Equity-Related Securities (2) - | | | | | | | | | |

| 0.0% of net assets at value | | | | | | | | | |

| | | | | | | | | |

| Parabellum Acquisition Partners, LLC (3)(5)(8) | | | Specialized Finance | | | | | | |

| Holding company for Special Purpose Acquisition Company (SPAC) interests | | | | | | | | | |

| Membership Units (acquired 4/22/21) | (I) (L3) | | | | 693,151 | | $ | 2,923,003 | | | $ | 0 | |

| | | | | | | | | |

| Total Controlled Affiliated Equity and Equity-Related Securities (cost: $2,923,003) | | | | | | | | | $ | 0 | |

| | | | | | | | | |

| Total Investments in Publicly Traded Equity and Equity-Related Securities, Money Market Fund Securities, and Legacy Privately Held Equity and Equity-Related Securities (cost: $90,790,722) | | | | | | | | | $ | 59,894,478 | |

| | | | | | | | | |

| Derivative Securities - | | | | | | | | | |

| 0.7% of net assets at value | | | | | | | | | |

| | | | | | | | | |

| Unaffiliated Derivative Securities (2) - | | | | | | | | | |

| 0.0% of net assets at value | | | | | | | | | |

| | | | | | | | | |

| Magnolia Neurosciences Corporation (3)(5)(7)(8) | | | Pharmaceuticals | | | | | | |

| Developed neurodegeration therapeutics | | | | | | | | | |

| Warrants for the Purchase of Common Stock expiring 8/3/28 (acquired 8/26/21) | (I) (L3) | | | | 138,059 | | | $ | 112,854 | | | $ | 0 | |

| | | | | | | | | |

| OpGen, Inc. (3) | | | Biotechnology | | | | | | |

| Developing genomic analysis tools | | | | | | | | | |

| Warrants for the Purchase of Common Stock expiring 2/17/25 (acquired 5/5/15) | (I) (L3) | | | | 3 | | 785 | | | 0 | |

| | | | | | | | | |

| Total Unaffiliated Derivative Securities (cost: $113,639) | | | | | | | | | $ | 0 | |

| | | | | | | | | |

| Non-Controlled Affiliated Derivative Securities (2) - | | | | | | | | | |

| 0.7% of net assets at value | | | | | | | | | |

| | | | | | | | | |

| Potbelly Corporation (3)(11) | | | Restaurants | | | | | | |

| Operates a chain of sandwich shops | | | | | | | | | |

| Warrants for the Purchase of Common Stock expiring 2/12/26 (acquired 2/10/21) | (I) (L3) | | | | 80,605 | | $ | 224,849 | | | $ | 419,795 | |

| | | | | | | | | |

| Total Non-Controlled Affiliated Derivative Securities (cost: $224,849) | | | | | | | | | $ | 419,795 | |

| | | | | | | | | |

| Total Derivative Securities (cost: $338,488) | | | | | | | | | $ | 419,795 | |

| | | | | | | | | |

| Total Investments (cost: $91,129,210) | | | | | | | | | $ | 60,314,273 | |

| | | | | | | | | |

The accompanying notes are an integral part of these unaudited consolidated financial statements.

23

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| 180 DEGREE CAPITAL CORP. CONSOLIDATED SCHEDULE OF INVESTMENTS AS OF JUNE 30, 2023 (UNAUDITED) |

| | | | | | | | | |

| Method of

Valuation (1) | | Industry | | Shares/Units | | Cost | | Value |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Other Financial Instruments (12) - | | | | | | | | | |

| | | | | | | | | |

| Unaffiliated Rights to Payments (Illiquid) (2) - | | | | | | | | | |

| 2.9% of net assets at value | | | | | | | | | |

| | | | | | | | | |

| Rights to Milestone Payments from Acquisition of BioVex Group, Inc. (acquired 3/4/11) (3)(5)(7)(13) | (I) (L3) | | Biotechnology | | $ | 548,998 | | | $ | 548,998 | | | $ | 0 | |

| | | | | | | | | |

| Rights to Milestone Payments from Acquisition of TARA Biosystems, Inc. (acquired 4/1/22) (3)(5)(7)(14) | (I) (L3) | | Pharmaceuticals | | $ | 1,703,036 | | | 1,703,036 | | | 1,822,420 | |

| | | | | | | | | |

| Total Unaffiliated Rights to Payments (cost: $2,252,034) | | | | | | | | | $ | 1,822,420 | |

| | | | | | | | | |

| Total Investments in Publicly Traded and Privately Held Equity, Money Market Fund Securities and Equity-Related Securities, Derivative Securities and Other Financial Instruments (cost: $93,381,244) | | | | | | | | | $ | 62,136,693 | |

| | | | | | | | | |

The accompanying notes are an integral part of these unaudited consolidated financial statements.

24

180 DEGREE CAPITAL CORP.

NOTES TO CONSOLIDATED SCHEDULE OF INVESTMENTS AS OF JUNE 30, 2023

(UNAUDITED)

Notes to Consolidated Schedule of Investments

(1)See Note 2. Summary of Significant Accounting Policies: Portfolio Investment Valuations.

(2)Investments in unaffiliated securities consist of investments in which the Company owns less than five percent of the voting shares of the portfolio company. Investments in non-controlled affiliated securities consist of investments in which the Company owns five percent or more, but less than 25 percent, of the voting shares of the portfolio company, or where the Company controls one or more seats on the portfolio company’s board of directors but do not control the company. Investments in controlled affiliated securities consist of investments in which the Company owns 25 percent or more of the outstanding voting rights of the portfolio company or otherwise control the company, including control of a majority of the seats on the board of directors, or more than 25 percent of the seats on the board of directors, with no other entity or person in control of more director seats than us.

(3)Represents a non-income producing investment. Investments that have not paid dividends or interest within the last 12 months or are on non-accrual status for at least 12 consecutive months are considered to be non-income producing.

(4)D-Wave Quantum Inc., ("QBTS") was formed through the merger of D-Wave Systems, Inc., and DPCM Capital, Inc., a special purpose acquisition company (SPAC). D-Wave Systems, Inc. was a legacy private portfolio holding of the Company. The Company initially invested in D-Wave Systems, Inc. starting in 2008 and through 2014, acquiring various classes of preferred stock. While the shares of QBTS owned by the Company are registered, the Company entered into a lockup agreement with QBTS that prevented the Company from trading or hedging these shares until February 5, 2023. As of that date, the Company's shares of common stock of QBTS are no longer subject to lockup restrictions.

(5)The Company is subject to legal restrictions on the sale of all or a portion of our investment(s) in this company. The total amount of restricted securities held is $8,599,211, or 13.8 percent of net assets.

(6)The Company received LLC Interests of 1.25 percent in AutoTech Ventures Management I, LLC ("AutoTech") pursuant to an Administrative Services Agreement between us and AutoTech and due to us following the termination of a former employee of the Company. These LLC Interests were separate from the compensation received for providing the administrative services under the agreement that were paid in cash. The LLC interests have a capital percentage of 0 percent.

(7)These securities are held by the Company's wholly owned subsidiary, 180 Degree Private Holdings, LLC ("180PH"), which were transferred from the Company to 180PH in the fourth quarter of 2020. The acquisition dates of the securities reflect the dates such securities were obtained by the Company rather than the transfer date.

(8)Represents a non-operating entity that exists to collect future payments from licenses or other engagements, monetize assets for future distributions to investors and debt holders, or is in the process of shutting down and distributing remaining assets according to a liquidation waterfall.

(9)The Company invested in Nanosys, Inc. in rounds of financing that occurred in 2003, 2004 and 2005. In May 2021, Nanosys completed a restructuring of its capitalization table that resulted in shares of Series C and Series D Preferred Stock being converted into shares of Series A-2 Preferred Stock and Series E Preferred Stock being converted into shares of Series A-1 Preferred Stock. The date of acquisition listed reflects the date of this conversion rather than the date of our investment in the company.

(10)The Company received shares of Ravenna Pharmaceuticals, Inc., as part of the consideration of the acquisition of Petra Pharma Corporation.

(11)The Company is the Investment Manager of separately managed accounts ("SMAs") that owns shares of these portfolio companies. Under our investment management agreement for the SMAs, the Company has the right to control the votes of the securities held by the SMAs. The Company has voting ownership between 5 percent and 25 percent in these companies when the shares held by us and our SMAs are aggregated.

(12)Other financial instruments are holdings of the Company that do not meet the definition of a security or a derivative.

The accompanying notes are an integral part of these unaudited consolidated financial statements.

25

180 DEGREE CAPITAL CORP.

NOTES TO CONSOLIDATED SCHEDULE OF INVESTMENTS AS OF JUNE 30, 2023

(UNAUDITED)

(13)If all the remaining milestones are met, the Company would receive approximately $4.1 million. There can be no assurance as to how much of these amounts the Company will ultimately realize or when they will be realized, if at all.

(14)If all the remaining milestones are met and the time-based payments are completed, the Company would receive approximately $4.6 million. Of this amount, approximately $1.3 million is due to be paid to the Company on April 1, 2024. There can be no assurance as to how much of the milestone-based payments will ultimately be realized or when they will be realized, if at all.

The accompanying notes are an integral part of these unaudited consolidated financial statements.

26

180 DEGREE CAPITAL CORP.

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

(UNAUDITED)

NOTE 1. THE COMPANY

180 Degree Capital Corp. (including its wholly owned subsidiaries the "Company," "us," "our" and "we"), withdrew its election to be treated as a business development company on March 30, 2017, and subsequently returned to its prior status as a registered non-diversified closed-end management investment company ("Closed-End Fund" or "CEF") under the Investment Company Act of 1940 (the "1940 Act"). We operate as an internally managed investment company whereby our officers and employees, under the general supervision of our Board of Directors, conduct our operations. As of May 22, 2020, we are also registered with the Securities and Exchange Commission as a Registered Investment Adviser under the Investment Advisers Act of 1940 (the "Advisers Act").

180 Degree Private Holdings, LLC ("180PH"), is a wholly owned limited liability company that was created in October 2020 to hold certain of the Company's securities of privately held companies. 180PH was consolidated for financial reporting purposes and is a disregarded entity for tax purposes under the Code.

180 Degree Capital BD, LLC ("180BD") was a 100 percent owned subsidiary of the Company that was sold to an unrelated buyer and the transaction closed in February 2023. 180BD was registered by the Company as a broker-dealer with the Financial Industry Regulatory Authority ("FINRA") that was formed to provide services to the Company related to fundraising for co-investment funds and not for investment returns. Historically, the Company consolidated 180BD for financial reporting purposes.